{kind=link}

Chinese stories always have something epic about them. They are full of adventure, unwavering loyalties, and characters (mostly male) who shoulder the fate of an entire nation. For example, in Romance of the Three Kingdoms, a classic by the medieval poet Luo Guanzhong (1330-1400), three men, fed up with the corruption of the empire, gather in a peach orchard and swear to rescue the people without fear of losing their lives. “Although we were not born on the same day, may Heaven and Earth grant that we die together,” says one of them. That afternoon, they slaughter an ox and celebrate. Perhaps that is why Chen Jinghe’s story could not be less than extraordinary. It is said that four decades ago, when he had recently graduated as a geologist from Fuzhou University, a Beijing official approached him with a simple yet monumental order: “Go to the mountains and find gold.”

Chen Jinghe didn’t ask questions. He climbed Zijin Mountain, in southeast China. After several explorations, along with a team of experts, he discovered a gold deposit — the largest in the country — and a copper deposit in the lower part of the mountain range. The then-young geologist was awarded the First National Prize for Scientific and Technological Progress and founded Zijin Mining. Today, he is the chairman of the board and CEO of a company that has expanded worldwide and has experienced one of the most rapid growths in the mining sector, with a market capitalization value of more than $75 billion, five times more than just five years ago.

This has helped consolidate its position within the small group of companies that control global production of critical minerals. This select club includes giants such as the British-Australian BHP and Rio Tinto, Brazilian Vale, Swiss Glencore, U.S. companies Albemarle and Freeport-McMoRan, the U.K.’s Anglo American, and Chile’s Codelco. Other Chinese firms include Zhejiang Huayou, Tianqi Lithium, China Northern Rare Earth, and CMOC, which are fighting back, redefining the global raw materials supply chain.

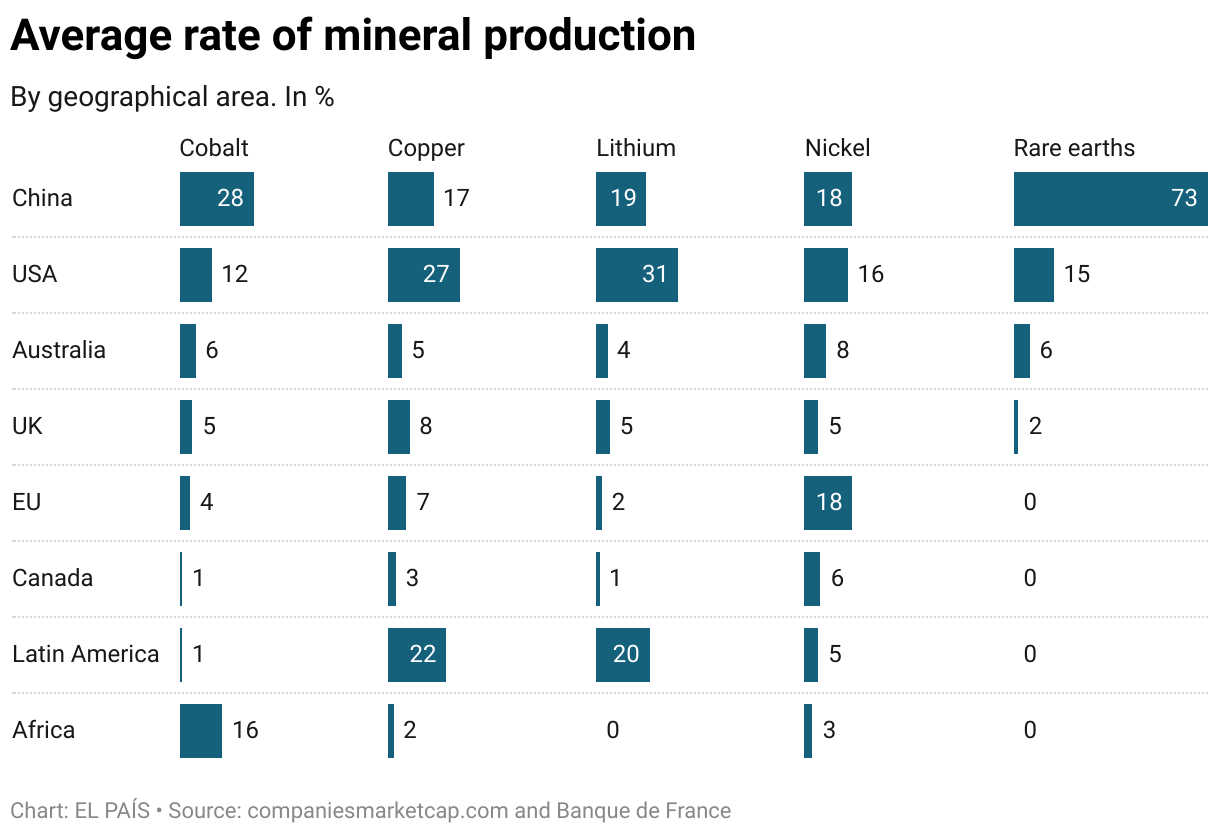

The sustainable and electric future lies in the grasp of a handful of companies. A small group of multinationals controls a large part of the production of critical minerals that are fueling the energy transition. Around 20 companies dominate this strategic and booming sector. Concentration varies depending on the material and the link in the value chain. For example, four firms account for approximately 55% of global cobalt production.

The situation is even more pronounced for lithium, where the top five control 80% of global production, according to a report by the French Central Bank called “Capital in the 21st Century: Who Owns the Capital of Companies Producing Critical Raw Materials?” The figures are roughly similar for other critical products such as copper, where five corporations also hold almost a third of the global market share. In a world marked by geopolitical disputes, concentration impacts competition and limits the entry of new players.

The major players, however, have no limits: they seek to become increasingly stronger against Asian companies, which have taken a significant bite out of the market. For example, China’s CMOC and Huayou have overtaken Glencore and positioned themselves as the dominant players in cobalt. “CMOC’s production capacity (120,000 tons) is now almost three times that of Glencore (38,200 tons), and Huayou’s cobalt production will reach 49,000 tons by 2024,” explains James Willoughby, an energy transition and battery materials expert at Wood Mackenzie.

CATL, the world’s largest manufacturer of electric vehicle batteries with a 35% market share, has vertically integrated into the supply chain by investing alongside CMOC in the Kisanfu project in the Democratic Republic of the Congo. In this alliance, CATL holds a 25% stake and CMOC 75%. Last year alone, the deposit produced more than 70,000 tons of this material, which is needed for the lithium-ion batteries used in electric cars such as the Tesla Model Y — the best-selling electric vehicle in the European Union (EU) — and the Ford Mustang Mach-E, one of the most popular plug-in vehicles in the United States.

“CMOC is perhaps Glencore’s most direct competitor,” say experts from the consulting firm CRU. CMOC is a giant founded in 1969 thanks to the efforts of the Chinese state to develop the mining industry in the central province of Henan. Its initial operations revolved around the extraction of molybdenum, an element used in steel alloys to increase their strength. The company expanded steadily until the turn of the century, which led to its listing on the Hong Kong Stock Exchange in 2007.

Then came its international expansion: it acquired assets in Australia (copper and gold), in Brazil (a niobium and phosphate business belonging to Anglo American), and has invested more than $9 billion in the Democratic Republic of the Congo between acquisitions, expansions, and associated agreements, according to Bloomberg estimates. It is in this material that it has placed its greatest efforts to become a global leader. But today the market is in decline. There is tepid demand in the electric vehicle segment (which demands less metal than a couple of years ago) and a geopolitical conflict over control of this raw material, whose price has fallen to historic lows due to excess supply.

Since the beginning of the year, Congolese President Félix Tshisekedi has restricted exports with the aim of boosting international cobalt prices. His intention is to regain some control over a strategic resource whose marketing is largely in the hands of CMOC, which regulates the market by adjusting its production as it sees fit.

The copper battle

Cobalt, also used in aerospace alloys and the petrochemical industry, is typically a byproduct of copper mining, and it is in the extraction of this material that CMOC wants to wage a new battle. Among the various critical materials (from certain rare earths to battery-related minerals such as nickel, cobalt, and lithium), this pinkish-orange metal is the most important in the electrification process of our economies, emphasizes Charles Kirby, partner in the Sustainability Consulting practice at EY Spain. “The largest absolute investments will be allocated to copper,” he adds.

This lustrous metal, says Ed Conway in his book Material World (2024), is both a symbol of our ancient history and a key to our future. “There is no other material that can match it,” the author believes. It is unique: it is a good conductor of heat and electricity, has natural ductility (it can be coiled, pulled, and made into wires without breaking), and is strong (it resists corrosion). “If steel is the skeleton of our world and concrete its flesh, copper is the nervous system of civilization,” Conway adds.

That’s why giants like BHP are converging on this product. Not only is it the world’s largest mining company by market capitalization, but it’s also the one that has put the most effort into staying at the top of the rankings and surpassing the U.S.-based Freeport and Chile’s Codelco. Furthermore, unlike other critical materials, there is room for growth. This is not the case in the rare earths sector, where China, with its two state-owned companies (China Rare Earth Group and China Northern Rare Earth Group), controls 73% of global production.

BHP is undergoing a transformation. It aims to move from being a predominantly iron ore company (essential for steelmaking) to a copper company. It is increasing its investment in this metal and anticipates that, in the coming years, it will account for a significantly larger portion of its investment, while its investment in iron ore will decline. It intends to make this shift with heavy financial backing. Last year, BHP and Lundin Mining acquired Filo Corp and its Filo del Sol and Josemaría projects, which straddle the border between Argentina and Chile. It has spent approximately $3 billion on them. The largest unconventional copper discovery in three decades has been announced there, which could reshape the global mining landscape and open up new exploration areas. “To maintain its position in the copper market, the company will have to continue investing,” notes Adam Webb, head of battery materials provisions at Benchmark Mineral.

BHP — whose largest customer is China, with approximately 60% of sales in the previous fiscal year coming from there — tried to pull out all the stops when it sought to acquire rival Anglo American (one of the oldest such companies in the world) in May. Its final offer of $49 billion — which has been hailed as one of the largest mining deals in history and would have created a firm with control of 10% of the global copper market — was effectively moot after being rejected by Anglo’s board. This, however, signaled a possible consolidation in the sector, at least among Western giants. Earlier this year, it was reported that Rio Tinto, the third-largest mining company in the world (behind only coal giant Shenhua Energy), and rival Glencore were discussing a merger of their businesses, although neither company confirmed the talks. This is not the first time these two titans have sought to join forces. In 2014, the Swiss company proposed a business alignment, but Rio Tinto rejected the offer.

Rio Tinto — one of the largest exporters of iron ore and aluminum — had until recently been focused on divesting its coal-related businesses and is now seeking to expand its focus into lithium. Last year, it acquired Arcadium Lithium for over $6.7 billion, which combines its assets in Serbia and Argentina. This acquisition follows its purchase of Rincon Lithium in 2022. Similarly, the company announced it will invest $900 million in the Salar de Maricunga project, a Codelco-controlled project in Chile. By 2035, these undertakings would make the company the second-largest player in this commodity, according to estimates by Benchmark Mineral.

Synergies

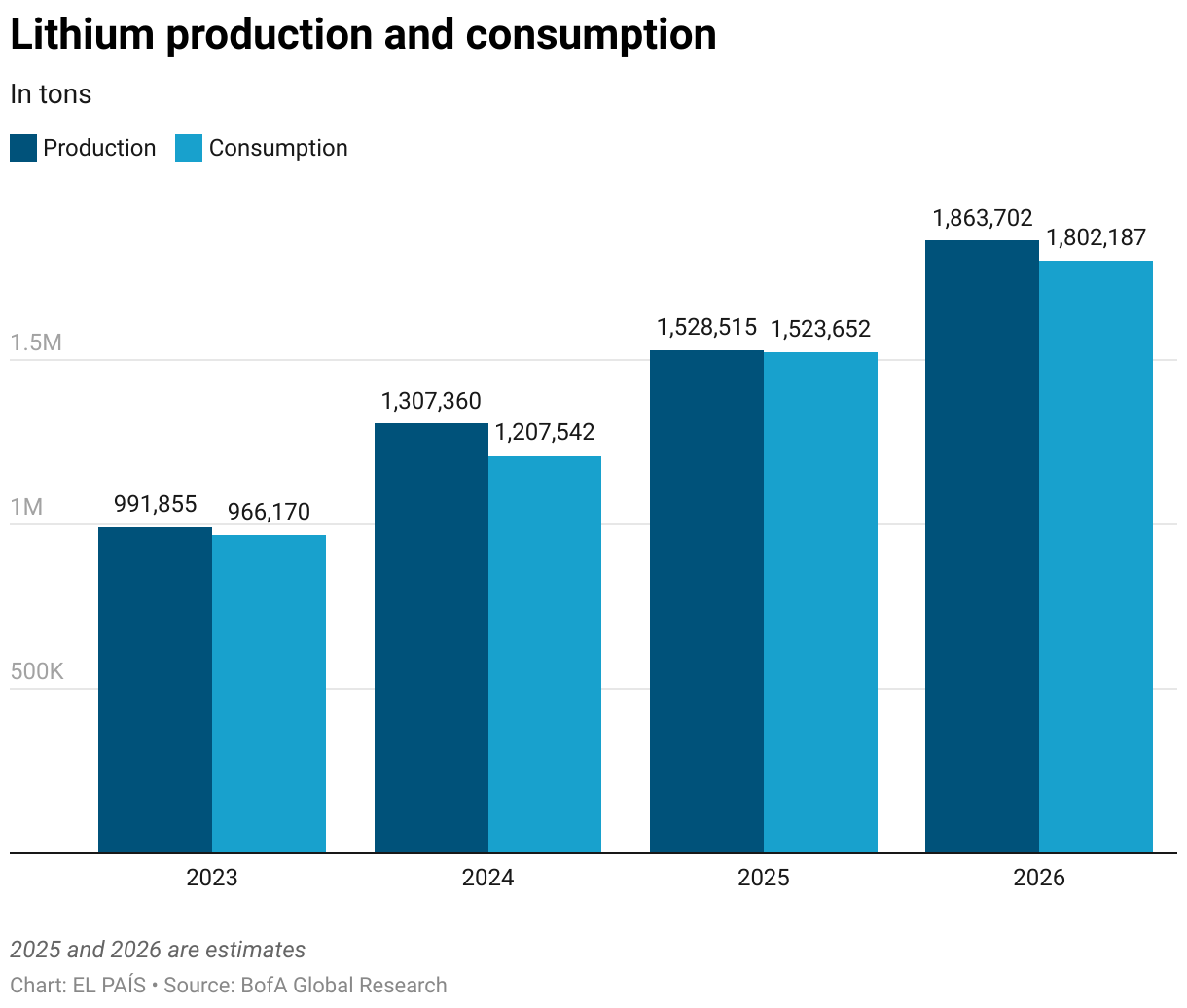

The strength of Rio Tinto and Codelco creates a positive synergy, according to experts, as they could generate opportunities in a crisis-hit market. “The key for BHP and Rio is to continue controlling large-scale, low-cost operations,” say experts from the consulting firm CRU. “This allows them to grow organically while also pursuing large-scale acquisition opportunities, such as Anglo American’s operations.” A key advantage of buying an existing business is that it eliminates many of the technical and capital cost risks associated with building a new asset, adds Willoughby of Wood Mackenzie. In the lithium market, however, there is a paradox: demand is rising and prices are constantly falling.

The sharp expansion of supply from China, Indonesia, and the DRC has seen lithium prices plummet by nearly 90% in two years, triggering a crisis in the sector. This collapse has paralyzed initiatives, canceled alliances, and forced mid-sized companies to adjust their operations. However, large producers remain confident that the price will bottom out this year.

Albemarle — the U.S.-based company that is the world’s largest lithium supplier — has warned producers this year that they will face higher costs, which will cause them to lose money and ground. “There will be pressure for [some participants] to exit the market,” said Kent Masters, the company’s CEO, at an investor forum in May. The firm has also put the brakes on the construction of a lithium processing plant in North Carolina, a $1.3 billion project that sought to establish a Western lithium supply chain.

The idea, however, is decades late. Although the U.S. firm has been able to establish itself as a key player in the lithium market — thanks to its expansion in Chile and Australia — Chinese companies are moving forward with determination in a market where cross-alliances in deposits reflect a complex web of shared interests. For example, Albemarle controls 49% of Greenbushes, the largest lithium deposit on the planet; its rival Tianqi Lithium owns the remaining 51%.

In Chile — the world’s second-largest producer after Australia and ahead of the Asian giant — this corporation has acquired almost a quarter of SQM’s stake in Atacama. But the interdependence doesn’t end there: Tianqi also controls nearly 22% of SQM, the Chilean producer that exploits the Salar de Atacama — the lowest-cost source of lithium globally — where Albemarle also operates. Together, the Atacama and Greenbushes operations accounted for 27% of global lithium supply in 2024. Adding Albemarle’s stake in Chilean brine also increases its footprint to 32%. This strategic overlap shows how, despite geopolitical competition, the sector’s leading companies are tied by a network of capital that transcends borders.

Continued strong growth in sectors such as electric vehicles and battery energy storage systems will lead them to become even more intertwined or consolidated. “To keep pace with this growing demand, new supply will be needed in the coming years, and China alone does not have the resources to meet this demand,” says Webb of Benchmark Mineral. This means there will be opportunities for new market entrants to develop new critical mineral projects, if their deposits are of sufficient quality to be built and operated profitably, he adds. New players may also benefit from a geopolitical situation in which the U.S. and Europe seek to reduce their dependence on China, the specialist points out. “There is potential for new players to enter the scene,” confirms Tae-Yoon Kim, senior analyst at the International Energy Agency (IEA).

New mines

He adds that there will likely be a mix of investments in both the development of new mines and the expansion of existing ones, with the balance between the two largely depending on the specific mineral. “For more nascent markets like lithium, a greater portion of capital is expected to be allocated to opening new explorations to meet rapidly increasing demand,” he predicts.

In contrast, for more established markets like copper, a greater portion of investment could be directed toward expanding existing operations. The energy transition will be costly. The industry will need to invest $1.7 trillion through 2037 to ensure a sufficient supply of copper, cobalt, nickel, and other critical metals, according to EY estimates. “Resources will not only be needed for extraction, but also for processing and recycling,” says Kirby, an expert at the consultancy.

The future, however, holds significant challenges. “Resource nationalism will prevail over supply chain optimization in a geopolitically risky world,” PwC specialists emphasize in an industry report published in June. In recent months, a wide range of export control measures for these products have been announced amid a never-ending trade war.

For IEA experts, any disruption in the supply of critical minerals could have a significant impact on technology prices, inflation, the competitiveness of the manufacturing industry, and the economy in general. Chen Jinghe, CEO of Zijin Mining, maintains that the sector must be ready for “a cold winter.” Deglobalization and resource nationalism pose significant challenges, he explained in his annual address to employees. While this is happening, the global mining supercycle, driven by Chinese industrialization, has come to an end, he emphasizes. “The changes will profoundly impact the market.” And he warns: “When things get tough, the strong carry on.”

Ernest Scheyder: “Chinese mining companies use what I call an economic weapon”

Amid what appeared to be unusual, pale patches of land surrounded by a sea of darker rock, Jerry Tiehm — a botanist who spent his spare time collecting and examining species in Nevada — spotted a wildflower sticking close to the ground. It was almost weed-like. Its stems grew up to 6 inches tall. It had blue-gray leaves and pale yellow flowers. Tiehm collected some samples (which would later be sent to New York), set up his tent, and camped for the night beneath the vast expanse of the Milky Way.

It was 1983, and Tiehm had discovered a new plant. He named it Eriogonum tiehmii, or Tiehm’s buckwheat. The species takes root in a place known as Rhyolite Ridge, in the western United States, where a huge lithium deposit lies that promises to power more than 75 million electric vehicles, according to Pioneer, the company developing the project, which received the first approvals under the Democratic administration of Joe Biden and is continuing the process under Donald Trump. “What matters more, the plant or the lithium beneath it?” asks Ernest Scheyder, a journalist specializing in critical materials at Reuters and author of The War Below (2024), which appears among Financial Times’ best economics books.

“This is a story about a decision: build the mine or preserve the species?” the author says in an interview with EL PAÍS. “Today, the Western world faces that dilemma as the need for lithium, copper, nickel, rare earths, and cobalt — critical metals for the construction of solar panels, electric vehicles, batteries, wind turbines, and electronic devices — increases,” says Scheyder, who will publish the book in Spanish next year.

Question. The slogan “No to mining in my backyard” is gaining traction in the West, the great consumer of technology. Is it fair to consume more while ignoring the costs of the sector in the Global South?

Answer. I would say that the era of us expecting things to be there at the store when we go there, without thinking through how they’re produced and where they’re produced, is rapidly ending. If we’re not comfortable thinking about mining in our own countries, then is it fair for us to expect the production and processing of those materials to be in a country we may never visit, or never see, or never interact with? I think these are deeply important questions and we can’t be naive about them. For example, the whole world knows about child labor in the mines of the Democratic Republic of the Congo, which is horrible. But are we willing to say, okay, we’re going to have more cobalt mining in our own countries because of that? Tracing the cobalt that comes from child labor and then ends up in our phones is almost impossible. Companies like Apple and Microsoft have tried to track that supply chain and they have not been successful.

Q. Does the world need to build more mines?

A. According to the International Energy Agency in Paris, we do. We’re going to need a lot more mines to produce a lot more, especially copper, but also nickel, cobalt, rare earths, lithium, and many other things. The good news is, at some point, we’ll reach what’s called the circular economy: the idea that we can then recycle all these old electronics and reuse the metals inside them to produce new devices. And then maybe we won’t need more mines at all. No one knows for sure when that will happen. Some point to 2050, others to 2075. I’m hesitant to put a specific date on it, but what I do know is that at some point, we’ll get there. In the meantime, we’re going to need more mines. And that means we need to have these kinds of discussions. It’s not just black and white. It’s not just should we have more mines or should we not? What we need to ask ourselves is: what are the standards that we expect of the mining industry? Just because we’re saying, OK, we need to have more mines, doesn’t mean people get to dig a hole everywhere. Are there some places that are too special to mine? What should the standards be for mining?

Q. The Donald Trump administration will allow the construction of more mines.

A. The Trump administration has signaled they want more critical minerals production. Some of the executive orders from President Trump have mentioned recycling. We just need more details. And they also point out that we need to be more self-sufficient in the United States. But also, if we want these devices, we have to be thinking about where we get the building blocks.

Q. Do you think Western companies really have the potential to grow and compete against the advance of Chinese firms?

A. Over the past two years, and before, we’ve seen Chinese mining companies use what I call an economic weapon to great effect: overproduction, producing more nickel, more copper, more lithium than is currently in demand. When you do that, you decrease the price globally. And that means your Western rivals have to shut operations. A good example is nickel. Chinese nickel miners and processors are overproducing and so now BHP, the world’s largest mining company, had to shut its nickel mines in Australia. That’s crazy. How do you compete against that? One way would be to ask consumers to pay more for products made with minerals mined to higher standards. Because BHP meets much stricter standards. But are we willing to pay more for products that are built with environmentally friendly nickel? Many consumers aren’t. And many companies aren’t either. If a factory needs 1,000 components to build a car, it might not be willing to pay more for just one of them, even if it’s more sustainable. Now, some governments are taking action. Recently, the Trump administration decided to financially support a company called MP Materials, which specializes in rare earths and magnet manufacturing. Whether this strategy was a good one is debatable, but it’s keeping the company financially afloat, and in fact, its stock prices more than doubled.

Q. It seems that Western companies need the same thing as Chinese ones: more public resources.

A. Yes, it seems that way. And it’s ironic because, during the 19th and 20th centuries, the mining industry was very politically conservative and didn’t want anything to do with government. And interestingly, now we’re seeing that perhaps government and the mining industry need to work closer [together]. I’d be interested to see how that pans out.

Sign up for our weekly newsletter to get more English-language news coverage from EL PAÍS USA Edition