{kind=link}

Global risk sentiment has remained defensive, with US equities under pressure amid uncertain prospects for a near‑term resolution to the US–Iran conflict. Iran has formally rejected a US ceasefire proposal, while President Trump has threatened further escalation. The risk of a broader confrontation, including potential US ground involvement, cannot be dismissed. VIX has risen sharply, though it remains below the peaks seen in the early stages of the Russia-Ukraine war and the post‑“Liberation Day” tariff shock. This suggests markets may still be underpricing the tail risk of a more prolonged or escalatory conflict.

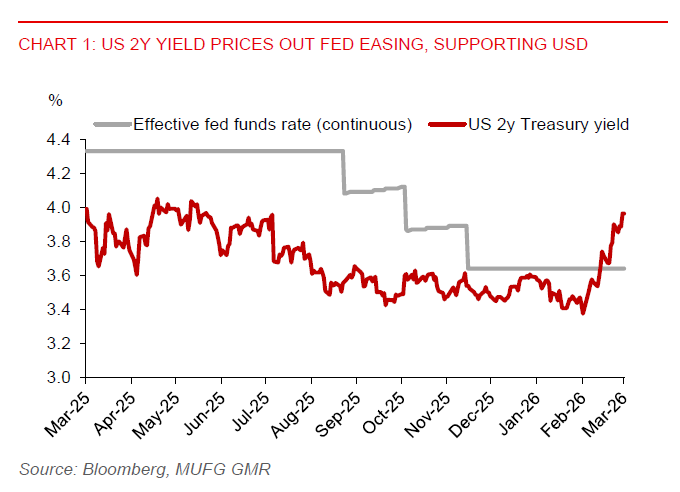

On rates, the current macro backdrop argues against any imminent Fed easing. The 2‑year Treasury yield is trading notably above the effective Fed funds rate. That said, the bar for outright hikes remains high in our view, given softer hiring momentum, growing fragilities in private credit, and widening credit spreads. “High for longer” US rates, against a backdrop of elevated geopolitical uncertainty and risk‑off equity markets, continue to underpin the USD, while keeping Asian FX on the defensive.

Regional FX

Our base case remains that the US–Iran conflict is relatively short‑lived and that the geopolitical risk premium eventually fades. However, the risk skew is towards a more prolonged conflict that keeps energy prices elevated for longer. In Asia FX, currencies with the highest energy import dependence remain the most exposed to further escalation in Middle East tensions, most notably KRW and JPY.

Elsewhere, PHP and THB also screen as highly vulnerable. In the Philippines, energy risks have moved squarely into the policy reaction function. BSP held an off‑cycle policy meeting following the government’s declaration of an energy emergency, though opting to keep rates unchanged at 4.25%. While growth remains weak and would ordinarily argue for easing, the energy shock has effectively priced out near‑term rate cuts. Markets are instead leaning towards the risk of hikes. With around 95% of crude oil imports sourced from the Middle East, the country is vulnerable to oil price and volume shocks. Against this backdrop, PHP remains highly sensitive to risk‑off sentiment and energy shocks.

The Thai baht has also underperformed sharply and is currently the weakest regional currency since the onset of the war. Thailand runs one of the largest net energy trade deficits in Asia, leaving its current account particularly exposed to sustained high oil prices. Funding costs for short THB positions remain low, making it a relatively attractive expression of energy‑driven risk‑off themes.