In a week marked by geopolitical tensions and fluctuating energy prices, the global markets have experienced mixed performances, with small-cap indices like the S&P MidCap 400 and Russell 2000 showing resilience amid broader market volatility. As investors navigate these uncertain times, identifying potential opportunities in undervalued small-cap stocks can be crucial, especially when insider buying suggests confidence in their future prospects.

Advertisement

Top 10 Undervalued Small Caps With Insider Buying Globally

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Eurocell | 11.4x | 0.3x | 47.35% | ★★★★★☆ |

| Lemonsoft Oyj | 19.3x | 3.0x | 43.14% | ★★★★★☆ |

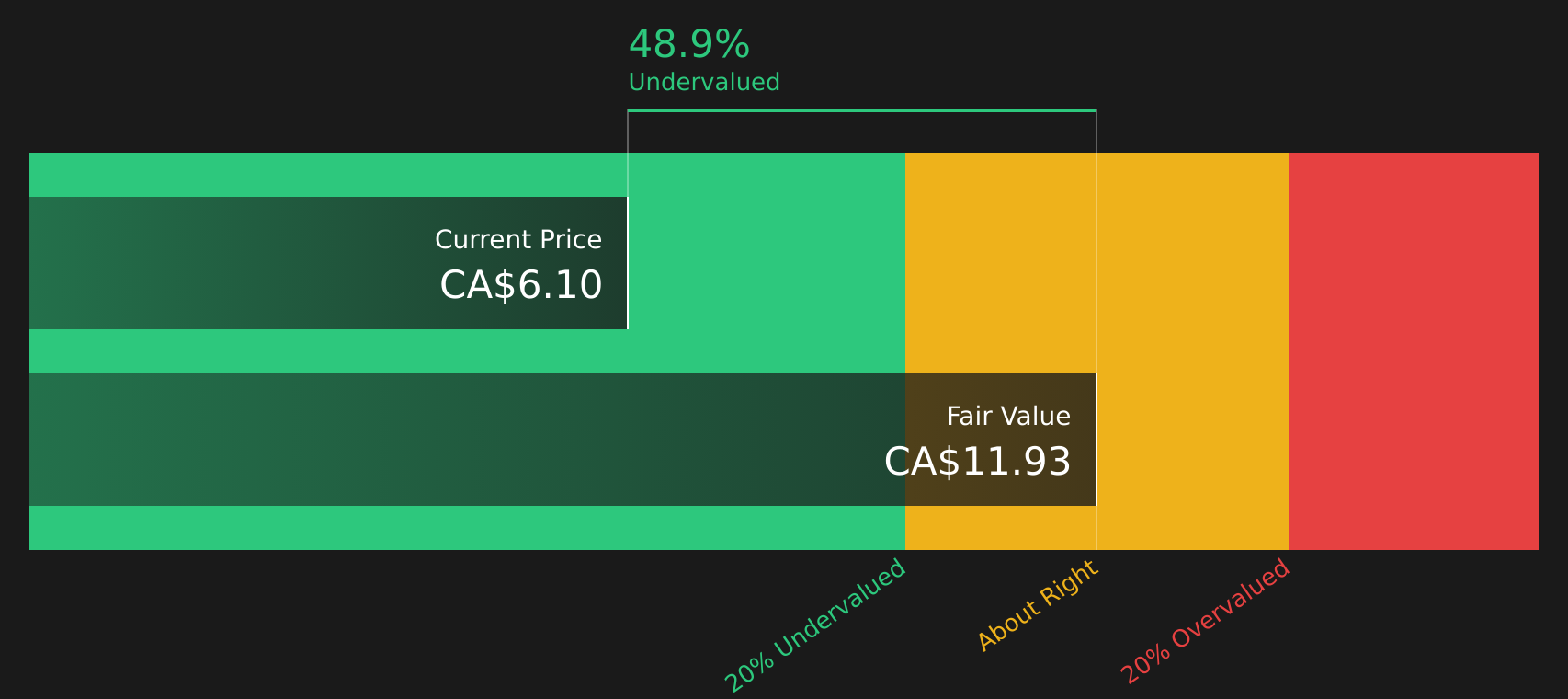

| Primaris Real Estate Investment Trust | 11.0x | 3.1x | 45.85% | ★★★★★☆ |

| Chorus Aviation | 7.0x | 0.4x | 46.69% | ★★★★★☆ |

| Centurion | 10.8x | 3.7x | -28.38% | ★★★★☆☆ |

| Eastnine | 9.2x | 6.2x | 21.29% | ★★★★☆☆ |

| Yellow Pages | 9.6x | 0.9x | 45.40% | ★★★★☆☆ |

| Cloetta | 18.4x | 1.7x | 21.85% | ★★★☆☆☆ |

| ASL Marine Holdings | 10.4x | 0.9x | -36.03% | ★★★☆☆☆ |

| Young’s Brewery | 39.9x | 0.9x | 42.29% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

Simply Wall St Value Rating: ★★★★★☆

Overview: Canfor is a Canadian company engaged in the production of lumber and pulp and paper products, with a market capitalization of CA$2.5 billion.

Operations: The company generates revenue primarily from its lumber segment, contributing CA$4.75 billion, and pulp and paper segment at CA$678.9 million. The gross profit margin has shown variability, reaching a high of 47.75% in mid-2021 before declining to 16.89% by the end of 2025.

PE: -2.0x

Canfor, a smaller player in the market, is navigating challenges with a recent net loss of C$390.5 million for Q4 2025 and asset impairments totaling C$321 million. Despite these setbacks, insider confidence is evident as they announced a share repurchase program on March 19, 2026, targeting up to 5% of outstanding shares by March 2027. Earnings are forecasted to grow annually by an impressive rate of nearly 75%, suggesting potential upside if operational improvements materialize.

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Savaria is a company that specializes in manufacturing and distributing products for personal mobility, including accessibility solutions and patient care equipment, with a market capitalization of CA$1.17 billion.

Operations: The company generates revenue primarily from its Accessibility segment, which includes adapted vehicles, amounting to CA$710.34 million, and the Patient Care segment contributing CA$203.19 million. The gross profit margin has shown an upward trend over recent periods, reaching 38.73% by the end of 2025. Operating expenses have been significant but are consistently managed within a range that supports profitability growth in net income margins over time.

PE: 27.3x

Savaria, a player in the accessibility solutions industry, shows potential as an undervalued stock with its recent financial performance. In 2025, sales reached C$913.53 million, up from C$867.76 million the previous year, while net income rose to C$68.77 million from C$48.51 million. Earnings per share increased to C$0.96 from C$0.68, reflecting strong operational growth despite higher-risk funding through external borrowing only. The company consistently declared monthly dividends of 4.67 cents (C$0.0467), signaling stability and commitment to shareholder returns amidst projected earnings growth of 20% annually over the coming years.

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Hemlo Mining is engaged in the exploration and development of gold and other precious metals, with a market cap of $426.07 million.

Operations: Hemlo Mining generates revenue primarily from the metals and mining sector, specifically focusing on gold and other precious metals. The company reported a gross profit margin of 40.13% as of September 30, 2025, reflecting an increase over previous periods. Operating expenses have remained relatively stable across the reviewed periods, with notable non-operating expenses impacting net income margins.

PE: 12.1x

Hemlo Mining, a small-cap company, is gaining attention due to its strategic initiatives and potential for growth. The recent executive changes aim to enhance operational excellence, while the 2025 gold production reached its highest in four years at 143,458 ounces. A disciplined exploration program has confirmed mineralization continuity at depth, promising long-term resource growth. Despite relying on external borrowing for funding, insider confidence is evident with share purchases in early 2026. Earnings forecasts predict a 20% annual growth rate, suggesting optimistic prospects despite current financial risks.

Seize The Opportunity

Ready For A Different Approach?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com