Advertisement

Why recent macro headlines matter for Wells Fargo

Recent headlines around bank exposure to nonbank financial institutions and Wells Fargo’s (WFC) own adjustment to its S&P 500 outlook have put big bank risk profiles back under the microscope ahead of earnings.

See our latest analysis for Wells Fargo.

At a share price of US$80.57, Wells Fargo has seen a 1 day share price return of 1.21%, while the 90 day share price return of 13.55% and year to date share price return of 15.37% point to fading near term momentum, compared with a 1 year total shareholder return of 13.92% and a 3 year total shareholder return above 7x that starting level.

If news around bank funding and FX services has you reassessing your watchlist, this can be a good moment to broaden your view with 20 top founder-led companies

With Wells Fargo trading at US$80.57 and referenced valuations suggesting a material intrinsic and analyst target gap, the key question is whether you are looking at a genuine discount or a stock where the market already credits future growth.

Most Popular Narrative: 7.9% Overvalued

According to mschoen25, the fair value for Wells Fargo sits at $74.70, which comes in below the last close of $80.57 and frames a tighter upside story than some headline targets suggest.

One of the reasons for its undervaluation is related to the broader economic environment, particularly the sluggishness in the housing and manufacturing sectors. However, Wells Fargo has significant advantages, such as a wide economic moat from its large customer base and low funding costs. Additionally, potential regulatory changes, like the lifting of the asset cap that limits the bank’s growth, could drive future profitability.

Curious how this narrative gets to a higher future earnings base and a richer profit multiple than today, even with only steady revenue growth baked in.

Result: Fair Value of $74.70 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this depends on a few pressure points, including any setback on lifting the asset cap and a weaker backdrop for housing or manufacturing credit demand.

Find out about the key risks to this Wells Fargo narrative.

Another View: DCF points to a very different story

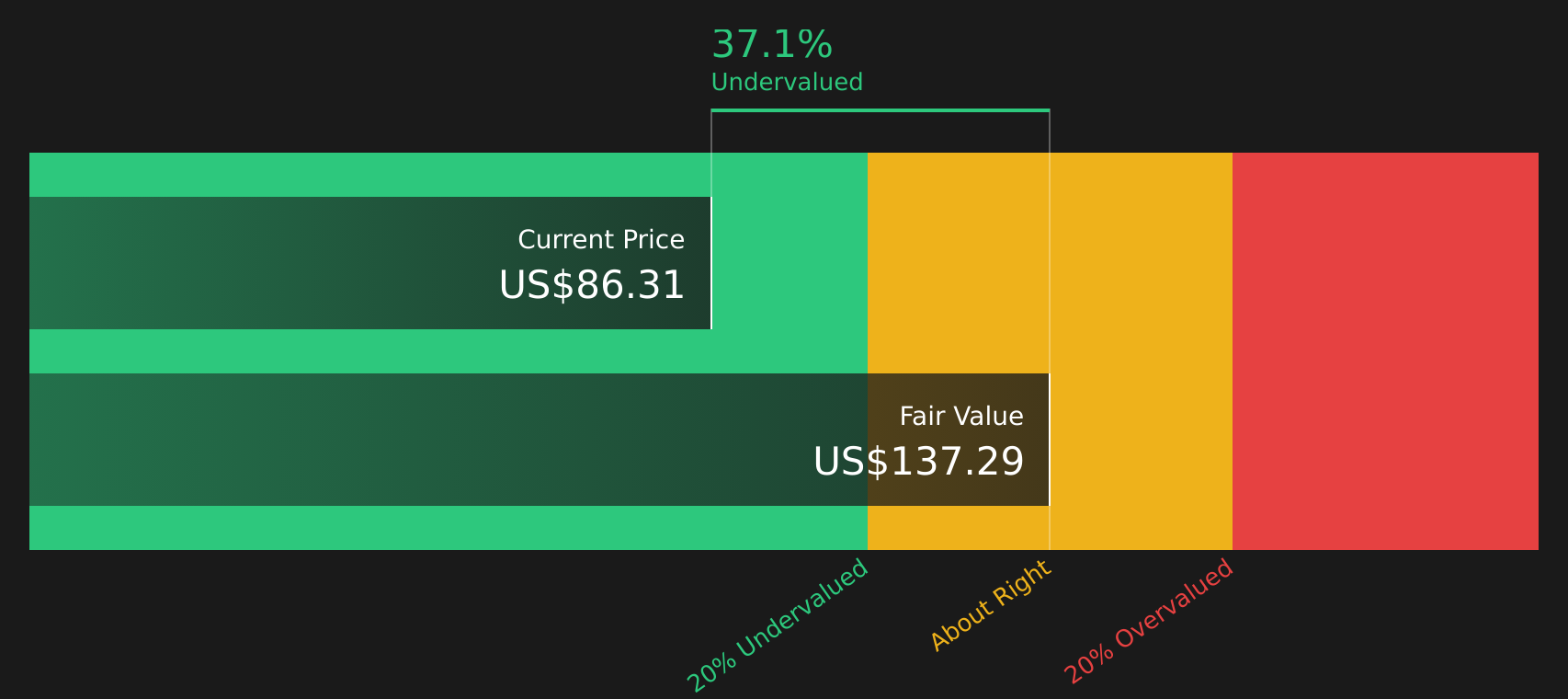

The user narrative pegs fair value at $74.70, slightly below today’s $80.57, which reads as 7.9% overvalued. Our DCF model, however, indicates an estimated future cash flow value of $128.28, suggesting Wells Fargo trades at a 37.2% discount. Which lens do you trust more for a long term view?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Wells Fargo for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 63 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

Mixed signals on value and risk can be a useful prompt to look closer at the details yourself and decide how comfortable you feel with the trade off. To pressure test both sides of the story quickly, start with the 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop with Wells Fargo, you might miss other opportunities that better fit your style, so widen your search now while these ideas are on your radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Wells Fargo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com