{kind=link}

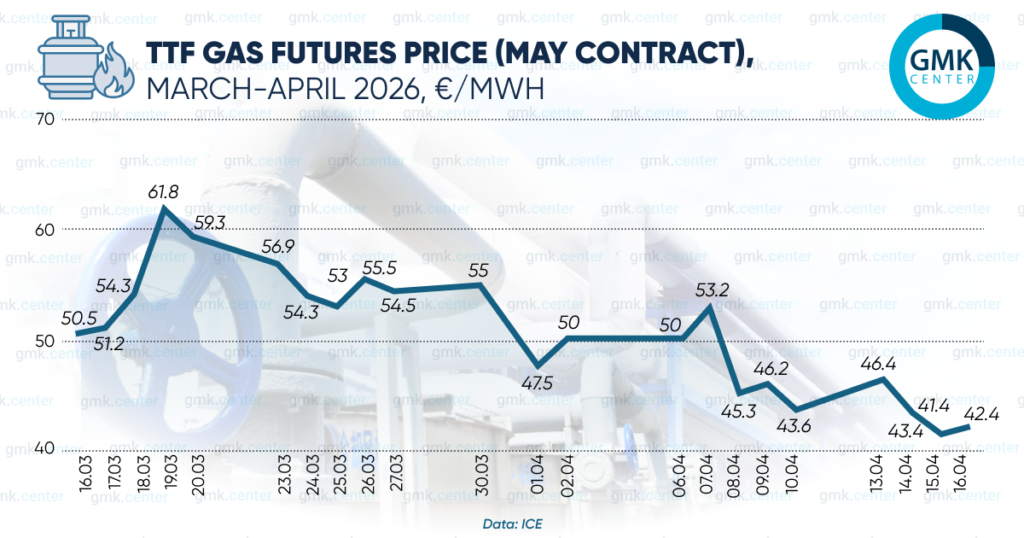

April prices fell significantly compared to the March high

In April, the European gas market continues to be driven more by political statements and uncertainty regarding the conflict in the Middle East than by fundamental indicators. However, April’s figures do not reach the highs seen in March.

For instance, on March 19, one-month TTF futures surged sharply after Iranian missile strikes damaged the world’s largest LNG export facility in Qatar—rising 24% from the previous day to €68/MWh, the highest price since late December 2022 (though it subsequently fell). At the time, QatarEnergy’s CEO stated that the attacks had knocked out about 17% of the company’s export capacity, and repairs would take three to five years.

The price increase was also driven by low fill levels in European gas storage facilities.

April TTF one-month-ahead futures prices fluctuated between €41 and €53/MWh in the first half of April. According to ICE, the highest price so far was €53.2/MWh on April 7.

Analysts note that the LNG market is tightening, but do not yet see insurmountable challenges in the EU’s preparations for the upcoming winter season.

ING analysts expect LNG supply disruptions to last longer, even if shipping through the Strait of Hormuz resumes quickly. In particular, it will take some time to restore Qatari production capacity.

The Asian and European gas markets, the financial group notes, are now bracing for tougher competitive conditions through 2027, as alternative supplies are scarce. Therefore, reducing gas demand will be key to balancing the market, a trend that is likely to be most evident in the energy sector.

Meanwhile, Ronald Pinto, an LNG analyst at Kpler, told Euronews that the company does not believe Europe is at risk of a gas shortage. Pipeline supplies to Europe remain normal, and LNG shipments are currently at the level observed in 2025.

Kpler believes that Europe will be able to import enough liquefied natural gas to start the next winter with sufficiently filled gas storage facilities, though at a much higher price than anticipated.

On April 9, the European Network of Transmission System Operators for Gas (ENTSOG) presented its summer supply forecast for 2026 at a meeting of the EU Gas Coordination Group, covering various scenarios regarding LNG availability in the coming months.

According to ENTSOG’s expectations, the infrastructure is ready to fill its storage facilities by at least 80% by November 1, depending on the availability of liquefied natural gas supplies. As noted, the EU gas system remains flexible and resilient thanks to new LNG regasification capacities (approximately 1,600 TWh) commissioned since 2022, and has the potential to compensate for lower storage levels at the start of the winter season.

ENTSOG indicates that as of April 1, 2026, EU gas storage levels stood at 28%, which is lower than in the previous three years and at the same level as before the energy crisis. The early start of injection—as early as April—and its continuation through November is a positive sign and will provide greater flexibility for filling storage facilities ahead of the next winter season.

According to the AGSI platform, as of April 17, 2026, European gas storage facilities were 29.56% full; last year, this figure stood at 36.1% on the same date.

It should be recalled that in the first half of March, the European gas market continued to be affected by the conflict in the Middle East.