Fortinet (FTNT) is under pressure after public disclosures of a critical FortiClient Endpoint Management Server vulnerability, now on key exploited lists, coincided with sector jitters about AI driven zero day discovery tools.

See our latest analysis for Fortinet.

The share price reaction to the vulnerability disclosures and AI driven threat concerns has come on top of weaker recent momentum, with a 1 day share price return of 4.91% decline and a 1 year total shareholder return of 21.52% decline. However, the 5 year total shareholder return of 86.16% shows the longer term picture has been more resilient.

If you are reassessing cybersecurity exposure after these headlines, it can be useful to scan a wider set of security and infrastructure names using our 36 AI infrastructure stocks

With Fortinet shares under pressure, yet trading at a discount to some analyst targets and certain intrinsic value estimates, the key question is whether current weakness is an entry point or if the market already reflects future growth.

Advertisement

Most Popular Narrative: 11.9% Undervalued

Fortinet’s most followed narrative pegs fair value at about $87.04, above the last close of $76.70, framing the recent pullback as a valuation gap the market is still debating.

Fortinet’s successful pivot toward high-margin, recurring software, subscription, and services revenue, evidenced by rapid ARR growth in Unified SASE (22%), SecOps (35%), and attached/adjacent cloud-based services, is structurally expanding gross and operating margins, decreasing business cyclicality, and boosting long-term earnings quality.

Want to see what kind of revenue mix, profit margins, and future earnings multiple need to line up to support that fair value gap and analyst targets.

Result: Fair Value of $87.04 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the story could change if the hardware refresh cycle fades without strong take up of newer services, or if heavy infrastructure spending fails to translate into sustained demand.

Find out about the key risks to this Fortinet narrative.

Another Angle On Valuation

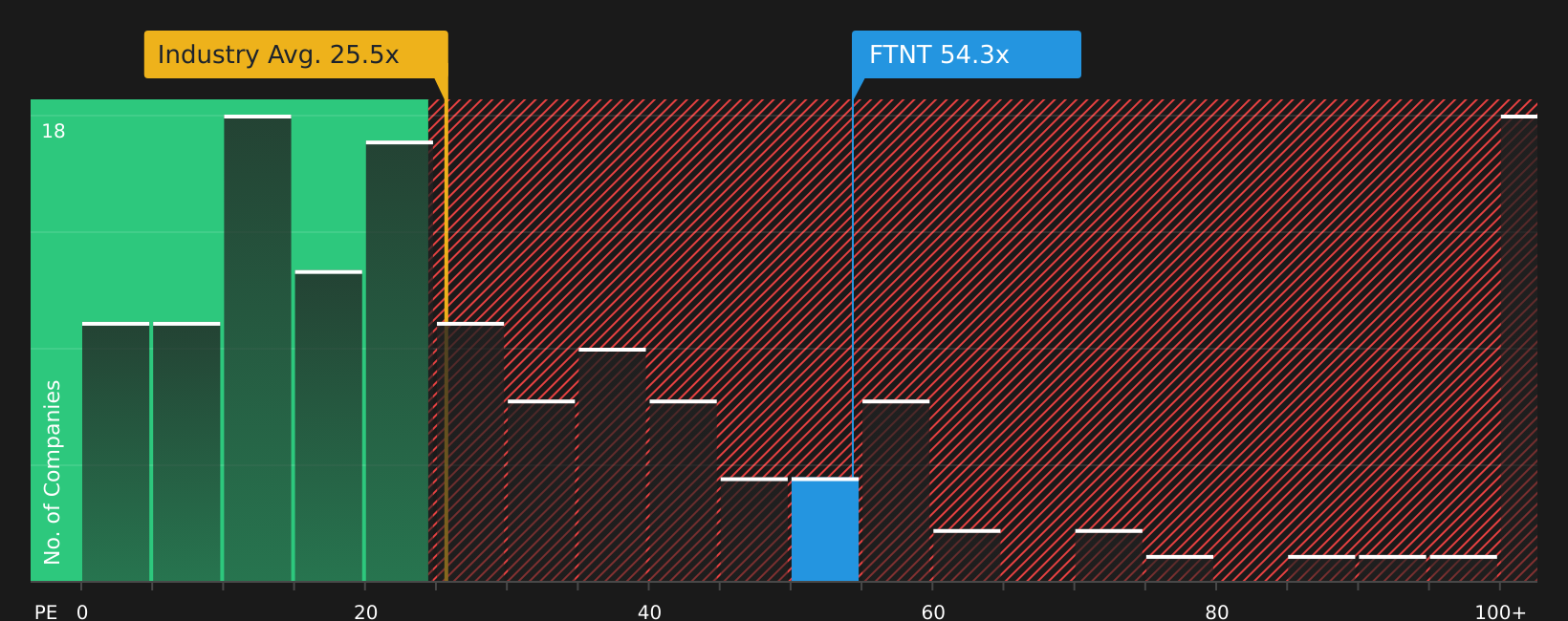

So far, the story leans on fair value estimates and analyst targets that suggest some upside. On plain earnings terms though, Fortinet trades on a P/E of 30.6x, above the US Software industry at 26.8x and roughly in line with its 30.6x fair ratio, which points to much tighter room for error than a clear bargain. Where does that leave you if sentiment weakens again?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this all feels mixed, that is exactly why the data matters. Move quickly and weigh it for yourself using the 3 key rewards.

Looking for more investment ideas?

Do not stop with one cybersecurity name when there are other potential opportunities across the market that could better match your goals and risk comfort.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com