{kind=link}

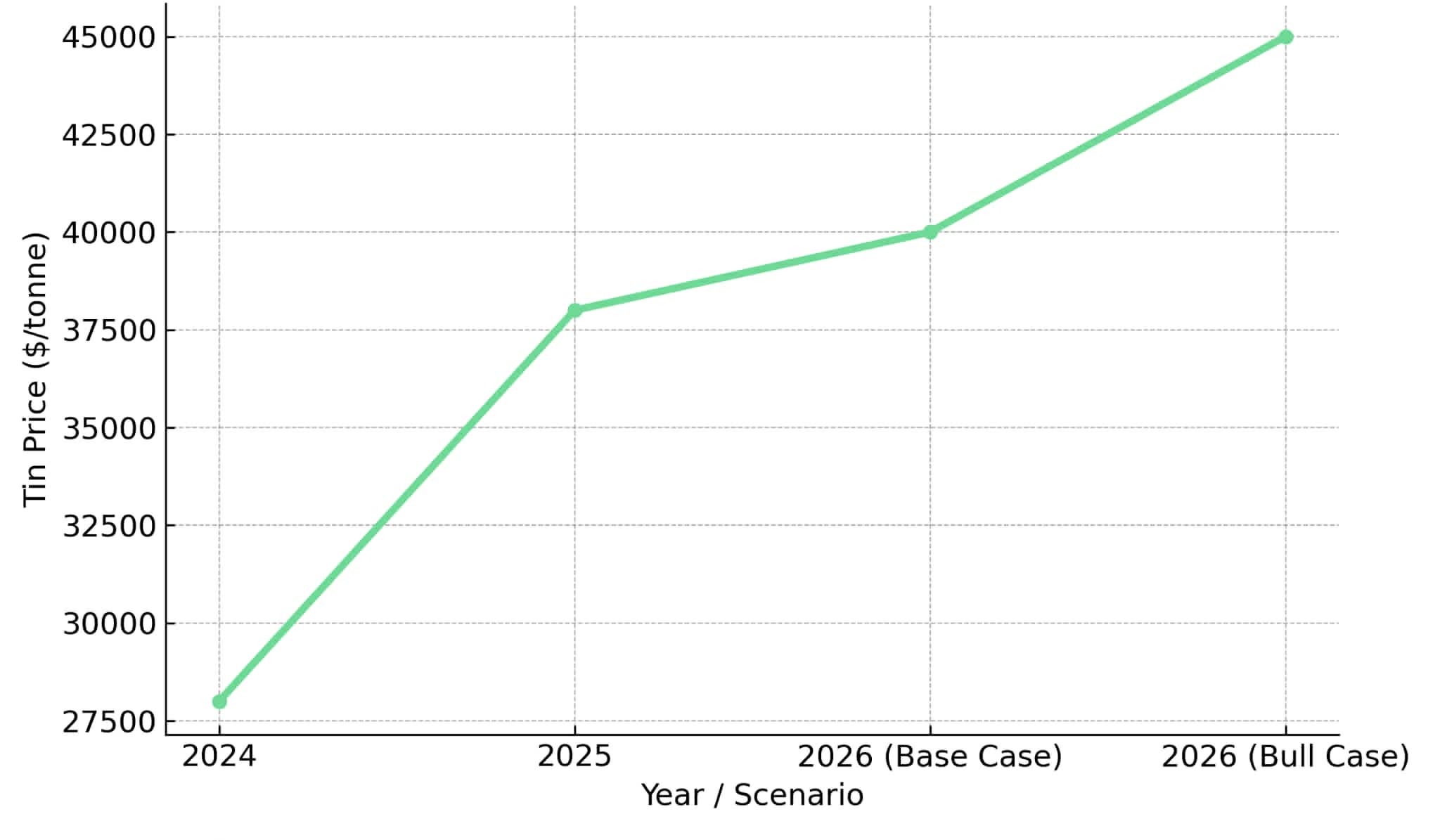

- Tin prices reached $38,000 per tonne in late November 2025, the highest in more than three years, driven by sharp supply disruptions in Myanmar and Indonesia.

- The tin market’s small size amplifies geopolitical risk, creating persistent volatility and strengthening structural deficits through 2026–27.

- Demand acceleration from electronics, electric vehicles, solar, and data center buildouts continues to outpace mine supply, reinforcing the long-term technology metal thesis.

- Development-stage companies with high-grade, scalable deposits, particularly those positioned near proven tin districts, are emerging as the most direct beneficiaries of the supply squeeze.

- Investors are beginning to reprice tin exposure as a scarcity-driven opportunity, with near-term catalysts concentrated on resource definition, permitting progress, and metallurgical validation.

Tin’s Price Breakout & the Macro Forces Behind the Three-Year High

Tin’s multi-year price high is not an isolated commodity cycle but the result of converging geopolitical, structural, and operational constraints. The November 2025 peak at $38,000 per tonne represents a decisive breakout, marking a year-on-year gain of 35.92% and a month-on-month increase of 5.62%. Unlike copper or lithium, where supply chains span dozens of major producers, tin’s concentrated production base creates inherent fragility. Myanmar, Indonesia, and select operations in Africa and South America account for the majority of global output, meaning disruptions in any single jurisdiction can rapidly tighten global balances.

Global tin consumption totals approximately 400,000 tonnes annually, magnifying price volatility when supply is constrained. A 50,000-tonne disruption represents more than 12 percent of global supply. This dynamic underpins the current price breakout: disrupted supply is meeting accelerating demand from electrification technologies, and the market has limited capacity to absorb shocks. Tin is experiencing a fundamental repricing driven by scarcity, geopolitical risk, and the metal’s essential role in advanced manufacturing.

Global Supply Disruptions Redefining Tin Price Dynamics

Geopolitical actions and operational halts have removed significant volumes from the global market at a time when demand growth remains robust. Tin is uniquely exposed to supply shocks due to its limited number of large-scale producers and concentration of output in jurisdictions with elevated regulatory or operational risk.

Myanmar’s Mining Suspension & the Structural Shock to Global Supply

The halt at the Man Maw mine, Myanmar’s top tin producer, due to a formal resource audit has removed critical volume from global supply. The suspension has been prolonged, with operations remaining halted as of late 2025. Myanmar’s tin output has historically provided low-cost, high-volume feedstock to regional smelters, particularly in China. The suspension coincided with rainy season conditions and infrastructure challenges that have complicated any potential restart timeline. No formal restart announcement has been made, leaving the market without clarity on when this supply will return. London Metal Exchange stockpiles have declined steadily throughout the second half of 2025.

Indonesia’s Regulatory Crackdown & the Supply Compression from Southeast Asia

Indonesian President Subianto’s order to close illegal mining operations in Sumatra has introduced a second major constraint on Southeast Asian tin supply. Indonesia is the world’s second-largest tin producer, and the resulting supply compression has tightened feedstock availability for licensed smelters and lowered overall output. Concentrate inventories at Indonesian smelting facilities have declined, reducing utilization rates and constraining refined tin output even as global demand remains firm. The Indonesian measures are expected to remain in place as the government prioritizes environmental compliance and formalization of the mining sector, creating a persistent constraint rather than a temporary disruption.

The Demand Engine: Electrification, Computing & Energy Transition Metals

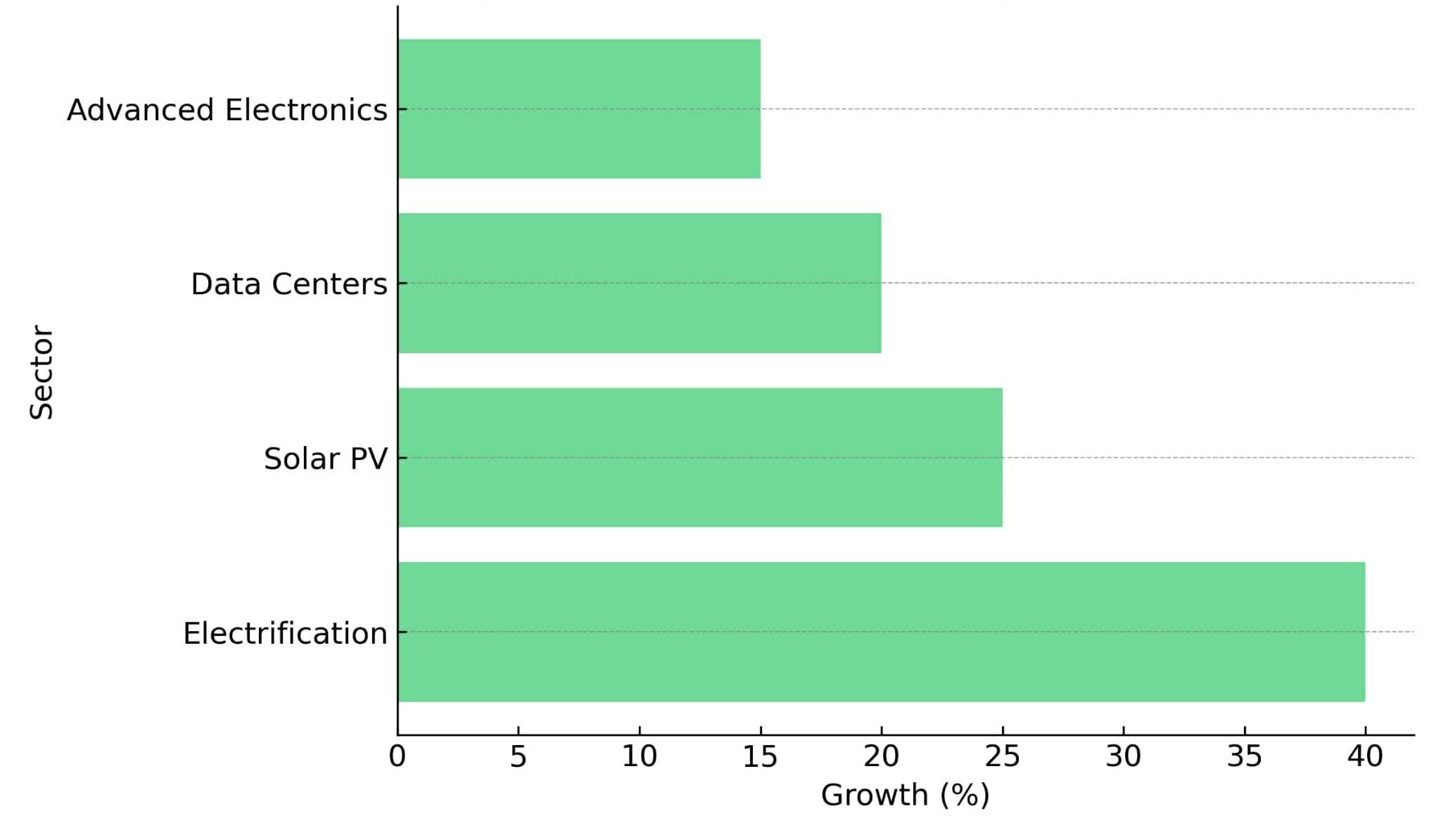

Tin’s core use in solder makes it essential to current electronics manufacturing, but the structural bull case emerges from demand acceleration in electric vehicle manufacturing, solar photovoltaic installations, global data centers, and advanced electronics. Tin-based solders are essential for battery management systems and power semiconductors in electric vehicles. Solar photovoltaic installations require tin-coated copper ribbons for cell interconnection. Data centers use tin solders extensively in server boards, networking equipment, and storage arrays.

Projections from the International Tin Association suggest tin demand could grow by up to 40 percent by 2030, driven primarily by these electrification and digitalization trends. This trajectory collides with constrained mine supply to create long-term deficits. New tin mines have been limited in number over the past decade, typical development timelines span five to ten years from discovery to production, and exploration budgets remain modest compared to copper or nickel. The result is a structural imbalance where demand growth outpaces supply additions, supporting higher long-term price decks and improving the economics of development-stage projects.

How Tight Markets Reframe Project Economics & Capital Allocation

Tin’s higher price deck directly impacts project economics by raising potential net present values, internal rates of return, and reducing payback periods for new developments. Exploration companies with high-grade ore bodies can achieve more favorable all-in sustaining costs and margin profiles when the price environment is supportive. A project that generates modest returns at $25,000 per tonne can become highly attractive at $35,000 per tonne, particularly if the deposit benefits from favorable metallurgy or proximity to existing infrastructure.

Investors reprice projects based on resource quality measured in grams per tonne of tin, metallurgical recoveries, infrastructure proximity, and jurisdiction. High-grade deposits near proven tin districts often command premium valuations because they reduce technical risk and demonstrate geological continuity with existing mines. Capital allocation in the tin sector is shifting as the macro environment validates the technology metal thesis, with development-stage companies attracting increased attention from both generalist commodity investors and specialized critical minerals funds.

Positioning of Development-Stage Companies in a High-Price Tin Market

Development-stage projects in established tin districts often command investor attention when global supply tightens. Companies advancing high-grade deposits, validating metallurgical pathways, or demonstrating geological continuity with producing mines are best positioned to benefit from the current macro environment.

High-Grade Districts & Why Proximity Matters

Rome Resources is advancing exploration targets in the Walikale Mining District in the Democratic Republic of Congo, positioned approximately 8 kilometers from Alphamin’s Bisie Mine and airstrip. Alphamin has demonstrated the geological potential of the district, with its Mpama South deposit grading 2 percent tin, substantially higher than the global average of 0.5 to 1.0 percent. Rome’s Mont Agoma and Kalayi exploration targets exhibit similar geological characteristics, with drilling results showing tin, copper, zinc, and silver mineralization.

The company operates from a permanent field camp that is fully serviced, with approximately 40 staff on site during full operations utilizing three active drilling units and an on-site core handling facility. Helicopter support enables access to the exploration targets. Rome maintains good relations with local inhabitants and artisanal miners operating in the region, reducing social risk and supporting future permitting processes.

Mont Agoma’s drilling program has returned encouraging results, including zones of tin mineralization that extend beyond the previously defined geochemical soil anomaly. Paul Barrett, Chief Executive Officer of Rome Resources, described recent exploration success:

“What we found with hole 30 which is down on the flank is a very good shallow tin zone. This is either a brand new zone or it’s a zone that’s been faulted in a kind of repeat sequence. Either way it’s pretty significant, especially considering that this lies outside the geochemical soil tin anomaly.”

Barrett emphasized the exploration upside, noting that the discovery suggests potential for resource expansion:

“The tin that we found is outside the tin anomaly so we think there’s a lot of scope now for the northeast flank of Mont Agoma.”

Proximity to Alphamin provides validation of the district’s geological continuity and reduces infrastructure risk. Rome’s exploration strategy leverages this proximity, targeting extensions and parallel structures that could host similar high-grade tin zones. The company is working toward an initial inferred resource estimate for its tin, copper, and zinc targets, having engaged MSA Group to prepare the resource work.

Metallurgical Pathways & the Economics of High-Grade Tin Development

Rome Resources shipped 1,000 kilograms of sample material to Canada for metallurgical and beneficiation testing during mid-2025. The testing program assesses recovery rates for tin, copper, and zinc, evaluates concentrate specifications, and identifies potential processing challenges. High-grade tin deposits generally benefit from simpler processing flowsheets and lower energy intensity per unit of metal produced, but metallurgical performance must be demonstrated. The results will inform future development decisions, including concentrate marketing strategies, infrastructure requirements, and capital intensity estimates.

Navigating Jurisdictional, ESG & Permitting Realities

The Democratic Republic of Congo hosts world-class mineral deposits, including significant tin, copper, and cobalt resources, though the sector has historically faced governance and infrastructure challenges. Geopolitical developments over 2024-2025 have contributed to evolving investor sentiment toward DRC mining projects. A recent agreement brokered by the United States includes access to minerals and is opening the DRC to new business. Alphamin is now majority owned by an Abu Dhabi sovereign wealth fund, demonstrating that institutional investors are willing to deploy capital in the region when asset quality and management teams meet investment criteria.

Barrett observed the shift in sentiment during recent investor meetings:

“I think the IR acquisition of Alphamin is showing that the outside world, I went to see the IR guys in Abu Dhabi in December and they said DRC, we’re not bought into it yet. Clearly they are now. I think the United States getting involved as well, it’s all positive for DRC critical minerals.”

Forward Supply Forecasts, Price Scenarios & Market Sensitivity Analysis

Forecasts from Trading Economics global macro models and analyst expectations suggest tin prices will average approximately $37,392 per tonne over the next quarter and reach $40,155 per tonne within 12 months. In a conservative scenario, Myanmar’s Man Maw mine returns to partial production within six months and Indonesian enforcement moderates, potentially stabilizing tin prices in the $32,000 to $35,000 per tonne range. The base case assumes continued supply constraints from Myanmar and Indonesia with steady demand growth, supporting prices in the $36,000 to $40,000 per tonne range through 2026. A risk-on scenario incorporates prolonged disruptions and accelerated demand from artificial intelligence data centers and electric vehicle adoption, potentially pushing tin prices above $45,000 per tonne.

The Investment Thesis for Tin

- Structural deficit trajectories emerge as supply disruptions from major producers coincide with rising electrification demand, creating a multi-year imbalance that supports higher tin prices and improves development project economics.

- Price resilience above $35,000 per tonne reinforces stronger project economics and reduces sensitivity to all-in sustaining cost variations, making marginal deposits more viable and attracting capital to the sector.

- Technology metal exposure positions tin as a critical electrification input with essential applications in solder for semiconductors, electric vehicles, and artificial intelligence data centers, linking the metal directly to long-term secular growth themes.

- Scarcity premiums are repricing development-stage assets near proven tin districts, particularly those with high-grade mineralization, favorable metallurgy, and geological continuity with existing operations.

- Geopolitical diversification through emerging jurisdictions supported by new international agreements may unlock alternative supply pipelines outside of traditional Southeast Asian production centers, reducing supply concentration risk.

- Rome Resources exemplifies the strategic positioning that attracts investor attention in a tight tin market, combining proximity to Alphamin’s proven high-grade district with polymetallic exploration targets, operational infrastructure including a permanent serviced camp and helicopter support, advancing metallurgical testing programs, and community engagement protocols that reduce permitting risk in an emerging jurisdiction benefiting from evolving geopolitical support.

What Tin’s Three-Year High Signals for Investors

Tin’s $38,000 per tonne breakout signals that supply uncertainty is structural, not temporary. Myanmar’s operational disruptions and Indonesia’s regulatory enforcement have removed meaningful supply volumes at a time when technology-driven demand continues to grow, tightening global balances and pushing prices to multi-year highs. Development-stage companies with high-grade deposits in proven tin districts are emerging as direct beneficiaries. The repricing of tin exposure reflects a broader recognition that supply additions in the sector are limited, timelines are long, and the macro backdrop supports sustained price strength. Tin represents one of the market’s more asymmetric setups over the next five years, offering superior risk-adjusted returns as scarcity premiums expand and structural deficits deepen through the remainder of the decade.

TL;DR

Tin prices reached a three-year high of $38,000 per tonne in November 2025, driven by supply disruptions in Myanmar and Indonesia that have removed critical volumes from global markets. The Man Maw mine in Myanmar remains suspended due to a resource audit, while Indonesia’s crackdown on illegal mining has tightened concentrate availability. These supply shocks coincide with accelerating demand from electric vehicles, solar installations, and data centers, creating structural deficits through 2027. The tin market’s small size—approximately 400,000 tonnes annually—amplifies volatility, with a 50,000-tonne disruption representing over 12 percent of global supply. Development-stage companies with high-grade deposits near proven tin districts are attracting increased investor attention as scarcity premiums expand. Projects positioned in emerging jurisdictions with operational infrastructure and advancing metallurgical programs are being repriced as strategic assets in a constrained supply environment.

FAQs (AI-Generated)