- In recent days, renewed geopolitical tensions around the Strait of Hormuz have reintroduced uncertainty over fuel availability, transport costs, and supply chain reliability for Royal Caribbean Cruises and other operators. This disruption risk is now a key operational consideration for the company, given its exposure to global fuel sourcing and broader sector sentiment.

- We will now examine how this heightened fuel and supply risk interacts with Royal Caribbean’s existing investment narrative and long-term outlook.

- We will now examine how heightened fuel supply uncertainty could reshape Royal Caribbean’s investment narrative and risk-reward balance for investors.

Capitalize on the AI infrastructure supercycle with our selection of the 38 best ‘picks and shovels’ of the AI gold rush converting record-breaking demand into massive cash flow.

Advertisement

Royal Caribbean Cruises Investment Narrative Recap

To own Royal Caribbean today, you need to believe in durable global cruise demand and the company’s ability to manage costs despite high leverage. In the near term, the key catalyst remains execution on pricing and bookings, while the biggest risk is cost inflation from fuel and operations. The latest tensions around the Strait of Hormuz raise fuel and supply uncertainty, but the impact on Royal Caribbean’s broader investment case is still emerging rather than clearly transformational.

The most relevant recent development here is the market’s mixed reaction to Royal Caribbean’s outlook, reflected in analyst revisions and a Zacks Rank of 4 (Sell) despite generally positive brokerage ratings. This split underscores how sensitive near term expectations are to execution, margins, and cost visibility, including fuel. As geopolitical news introduces fresh questions around fuel availability and pricing, those differing views on earnings power and valuation could widen further.

Yet beneath the strong brand and recent results, investors should be aware that rising fuel cost volatility could…

Read the full narrative on Royal Caribbean Cruises (it’s free!)

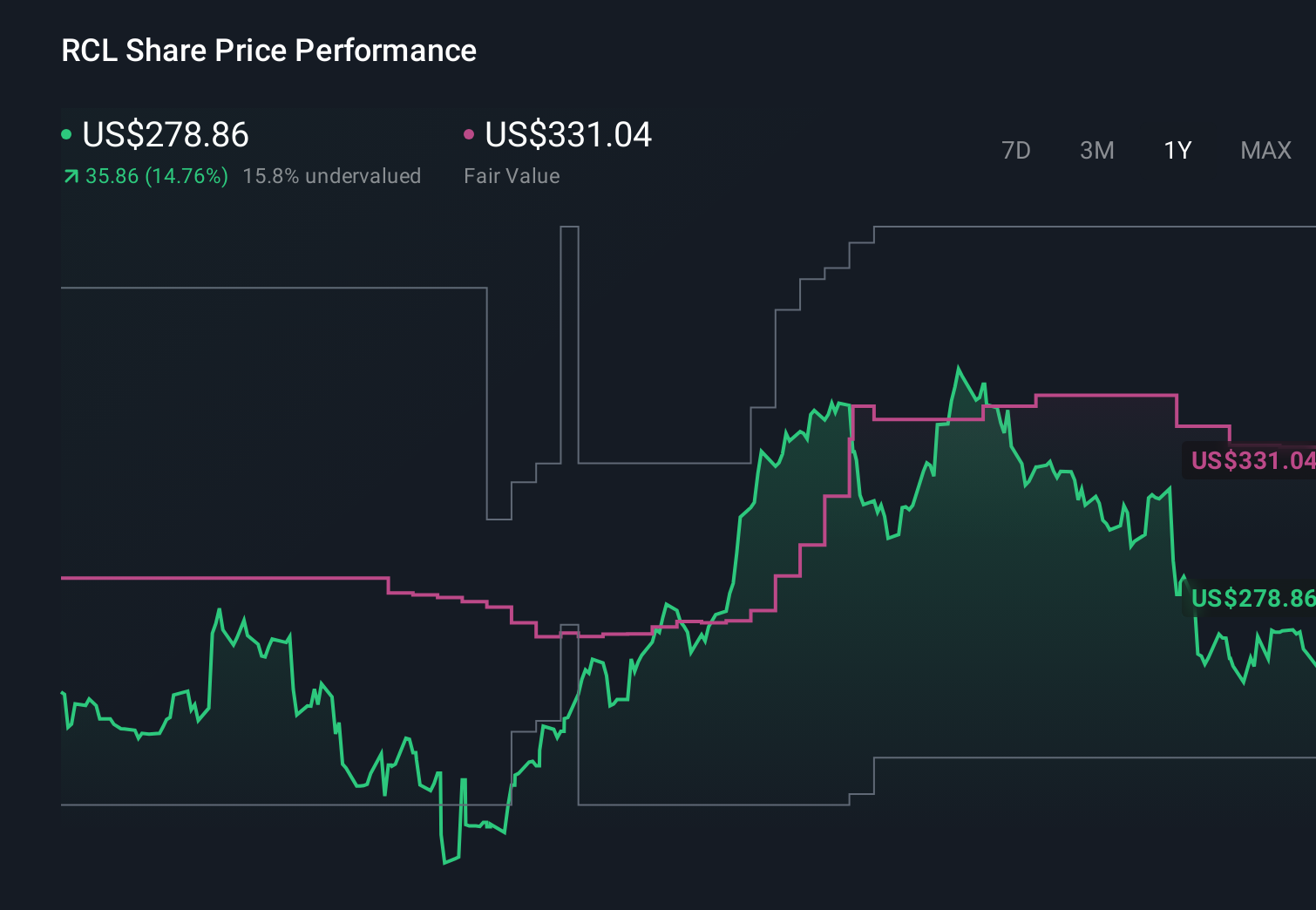

Royal Caribbean Cruises’ narrative projects $23.0 billion revenue and $6.1 billion earnings by 2029.

Uncover how Royal Caribbean Cruises’ forecasts yield a $348.46 fair value, a 34% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were projecting revenue near US$24.2 billion and earnings of about US$6.9 billion before this news, while also downplaying fuel cost risk, so you can see how their upbeat narrative might need rethinking compared with more cautious views that treat fuel volatility as a central concern.

Explore 6 other fair value estimates on Royal Caribbean Cruises – why the stock might be worth as much as 63% more than the current price!

The Verdict Is Yours

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

- A great starting point for your Royal Caribbean Cruises research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Royal Caribbean Cruises research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Royal Caribbean Cruises’ overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don’t delay:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com