{kind=link}

On April 8, the Dow Jones Industrial Average surged 2.8% in a single day, while oil prices plummeted 16%, marking the largest decline since the pandemic. However, the sustainability of the rebound remains uncertain: the ceasefire only lasts for two weeks, and the flow of tankers through the Strait of Hormuz remains a ‘key indicator.’ Internal divisions have also emerged at Goldman Sachs—while strategists believe that ‘a rebound is possible once the shock peaks,’ the head of trading openly stated ‘not to chase the rally’ and took the opportunity to reduce positions.

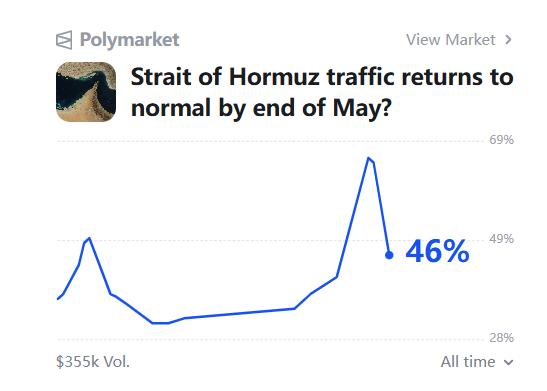

The missiles are still in flight, the strait remains closed, yet the market has already decided to celebrate first. However, amidst the jubilation, some have quietly begun reducing their positions.

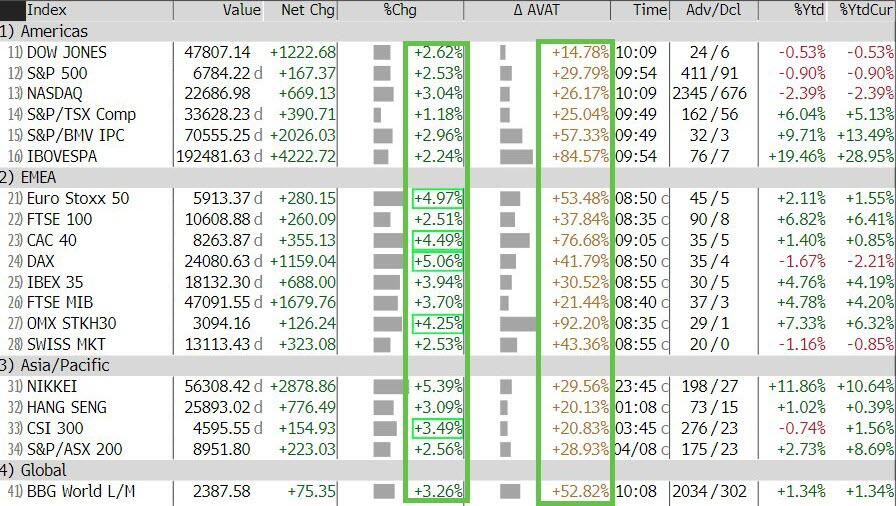

On April 8 Eastern Time, the news of a U.S.-Iran ceasefire agreement was announced, triggering an immediate and significant reaction in global financial markets. $Dow Jones Industrial Average (.DJI.US)$ The index surged by 2.8% in a single day, approximately 1,325 points, marking the largest one-day increase in over a year. $S&P 500 Index (.SPX.US)$ Up by 2.5%, $NASDAQ 100 Index (.NDX.US)$ Increased by 2.9%.

Major stock indices in Europe and Asia all recorded gains exceeding 2%.

Major stock indices in Europe and Asia all recorded gains exceeding 2%.

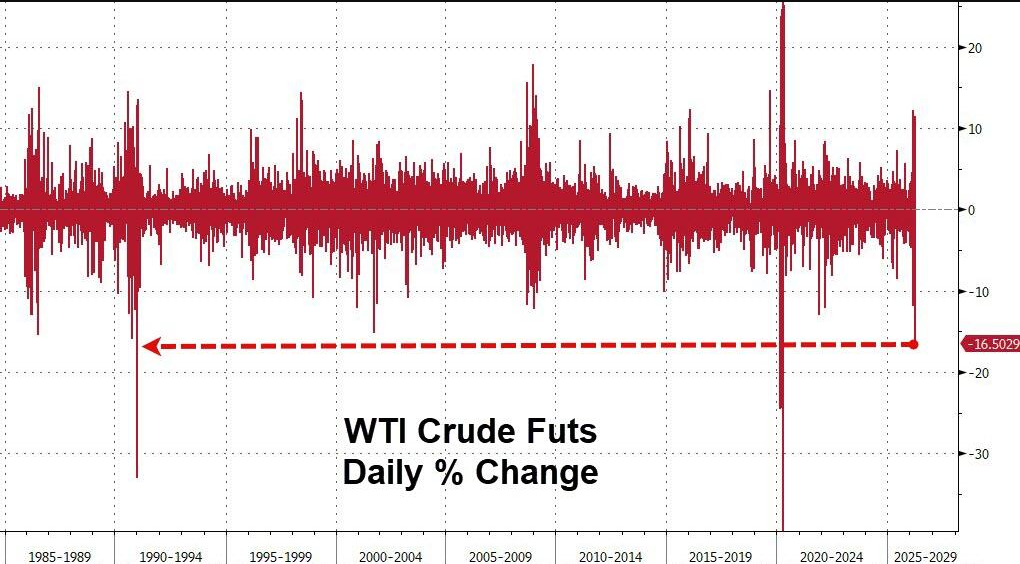

Meanwhile, the U.S. benchmark oil price $Crude Oil Futures (MAY6) (CLmain.US)$ Plummeted by 16% in a single day to $94.41 per barrel, representing the steepest decline since the COVID-19 pandemic and the largest one-day drop since the Gulf War in 1991.

However, this rally has been accompanied by unease from the outset. The ceasefire agreement is only for a two-week period, and tanker traffic through the Strait of Hormuz remains sluggish. Throughout the trading session, there were repeated reports of the ceasefire breaking down—Netanyahu declared, “This is not the end of the war,” while Iranian officials claimed that the ceasefire had been violated. Stock indices pulled back significantly from intraday highs, with closing gains sharply reduced compared to opening futures.

Phil Blancato, Chief Market Strategist at Osaic, stated: “The market has a pent-up demand for even the slightest positive news.” However, multiple market participants simultaneously warned that whether the ceasefire can hold and whether the strait can truly reopen to navigation remain the biggest uncertainties.

Rally Logic: Short-Covering + Emotional Release

The driving force behind this rally is less about fundamental improvement and more about mechanical adjustments in position structures.

According to data from Goldman Sachs’ trading desk, overall activity levels were 70% higher than the average of the past two weeks, but the intensity of short-covering fell below market expectations. Rich Privorotsky, Head of Goldman Sachs’ Delta-One business, noted that prior to this, the overall market position size was relatively high, with net positions being low. Investors generally held excessive index hedges, and a large number of futures short positions needed to be covered—this provided the primary fuel for the rebound.

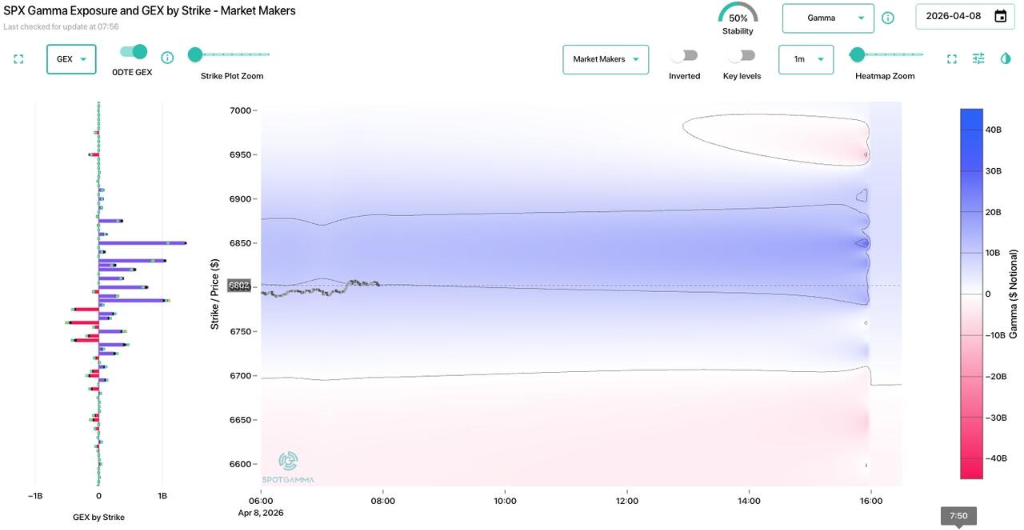

Mechanical buying driven by CTA strategies also kicked in, with volatility compression acting as a tailwind. According to SpotGamma data, there is a concentration of approximately $10 billion in positive Gamma near the S&P 500 level of 6800 points (at the 85th historical percentile). This structure propelled the index upward rapidly but also created resistance to further upside.

Goldman Sachs’ trading desk observed that long-only funds (LO) were the main force behind this round of buying, with net purchases ranking at the 87th historical percentile, primarily concentrated in technology and macro products. Hedge funds (HF), on the other hand, maintained a relatively balanced stance, even reducing positions in sectors such as technology and energy.

Market Divergence: Technology Leads Gains, Energy Suffers Heavy Losses

At the sector level, this rebound exhibited distinct characteristics of a ‘reversal of wartime logic.’

Economically sensitive sectors performed strongly across the board: industrial stocks, discretionary consumption, and homebuilders all saw significant gains. Flash memory manufacturer $SanDisk (SNDK.US)$ Surged by 9.9%, United Airlines climbed 7.9%, and the Dow Jones Transportation Average reached a record high. Goldman Sachs’ TMT Momentum Portfolio (GSTMTMOM) soared by 10% in a single day, marking its largest one-day gain in history and closing at an all-time high.

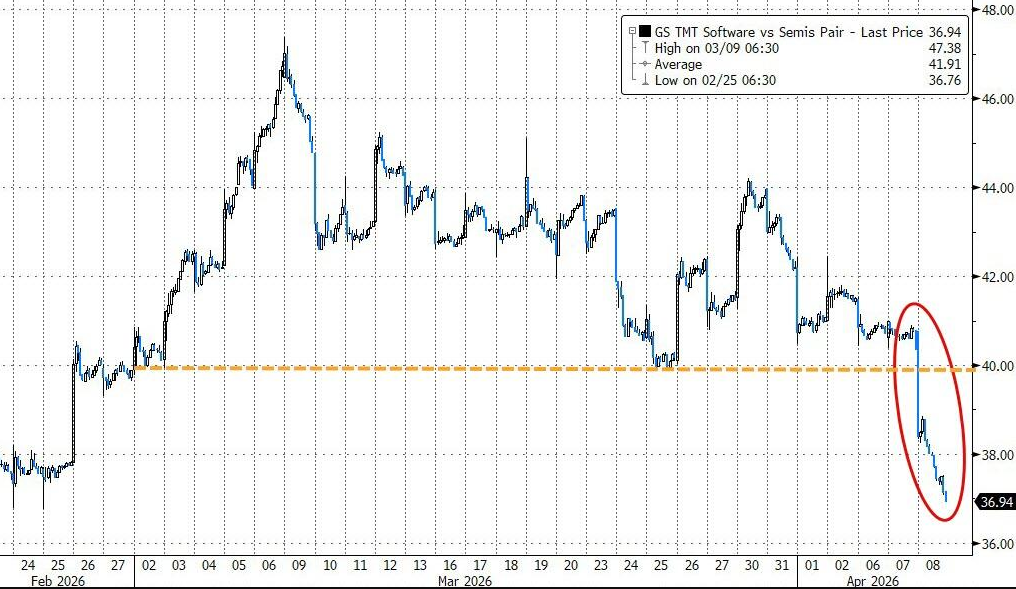

The energy sector, however, faced a reverse impact. $Exxon Mobil (XOM.US)$ 、 $Apache (APA.US)$ 、 $Cheniere Energy (LNG.US)$ Stock prices of companies such as Exxon Mobil fell, while U.S. fertilizer producers $CF Industries Holdings (CF.US)$ A decline of 5.7%. According to Goldman Sachs data, the relative strength portfolio of semiconductors versus software (GSPUSOSE) plummeted by 8.5% in a single day, also setting a historical record.

In the bond market, the initial ceasefire news triggered a sharp decline in global yields, significantly contracting market pricing for central bank rate hikes. However, selling pressure emerged during U.S. daytime trading hours, with the 30-year U.S. Treasury yield ultimately closing higher. The 10-year Treasury auction results fell below expectations, reflecting a decline in foreign demand.

Internal Disagreement at Goldman Sachs: A Rebound is Expected, but Chasing the Upside is Not Advisable

Faced with the same market conditions, Goldman Sachs internally expressed sharply differing views.

Dominic Wilson, Goldman Sachs’ Chief Cross-Asset Strategist, noted in a previous report that historical experience shows stock markets can rebound from their lows without waiting for crises to be fully resolved, requiring only confirmation that downside risks have peaked. He cited examples from the pandemic and tariff shocks: in both cases, equities bottomed out before economic pressures reached their peak. Wilson also pointed out that at a price-to-earnings ratio of 25 times, even if all earnings of the S&P 500 for an entire year were written off, the market would only fall by 4% — “an ambiguous resolution path” could still trigger a rebound.

However, Rich Privorotsky, Head of Goldman Sachs’ Delta-One business, held a contrasting view. He stated bluntly, “Chasing the upside at current levels is not a good trade.” He believed this rally was more of a technical rebound driven by short-covering rather than a fundamental improvement. The S&P 500 has recovered about two-thirds of its earlier losses, while European stock gains appear excessive — he estimated that a “reasonable” rebound should have been between 2% and 3%, rather than the actual recorded 5%.

Privorotsky’s operational choice was to sell part of his long positions amid this surge, rather than increasing his position.

The true arbiter: tanker traffic through the Strait of Hormuz

The core suspense of the ceasefire agreement lies in whether the Strait of Hormuz can truly resume navigation.

Iranian Foreign Minister Abbas Araghchi stated on social media: “Within two weeks, coordinated by Iran’s armed forces and taking into account technical limitations, secure passage through the Strait of Hormuz will become possible.”

Privorotsky’s interpretation of this phrasing is quite straightforward: tankers must receive approval from Iran’s ‘toll station’ to pass through, and ‘technical limitations’ mean that throughput will be actively controlled – ‘Supply will be sufficient to avoid escalation but not enough for Iran to lose leverage in negotiations.’ Based on this, he judged that international crude oil would remain in the $90 range rather than fall back to the $80 range.

According to the Wall Street Journal, tanker tracking agencies show that shipping volumes in the Persian Gulf remain far below pre-war levels. Neil Roberts, head of maritime and aviation at Lloyd’s Market Association, stated: “The likelihood of a simple normalization of tanker flows is extremely low.”

Clearview Energy Partners wrote in a client report that oil prices ‘failed to fall further after the ceasefire news due to sticky fundamentals, while the ceasefire agreement itself is fraught with uncertainties.’

Technical warning: historical ‘exhaustion gaps’

Noteworthy signals have also emerged on the technical side of the market.

Analyst @alpha_pls noted on X platform that the S&P 500 triggered a rare technical event that day – simultaneously gapping above both the 50-day and 200-day moving averages. Since 1950, this signal has occurred only four times, with significant pullbacks each time thereafter: the average maximum drawdown over the following three months was 9.51%, with the largest single pullback occurring in 2018 at 12.92%. The analysis pointed out that historically, this pattern has always been an ‘exhaustion gap’ rather than the start of a sustainable rebound.

Meanwhile, despite a significant drop in the Cboe Volatility Index (VIX) on the day, it remains above 20 and is notably higher than pre-war levels. Ben Emons, Chief Investment Officer at Fed Watch Advisors, stated: “This is a fragile situation that cannot be ignored. Market pricing indicates there is still demand for hedging, or markets are waiting for further clarity on developments.”

Mark Hackett, Chief Market Strategist at Nationwide, put it bluntly: “This is not something that can be resolved with a wave of a magic wand.”

The broader context: Economic pressures have not dissipated.

Even if a ceasefire agreement is ultimately sustained, the accumulated economic pressures will not simply disappear.

Oil prices are currently about 60% higher than at the start of the year, continuing to weigh on the U.S. economy, which is already facing stubborn inflationary pressures. According to CME FedWatch data as of April 8, traders now see a 73% probability that the Federal Reserve will not cut interest rates throughout 2026, compared to just 4% before the conflict erupted.

Wilson, Chief Cross-Asset Strategist at Goldman Sachs, noted that markets have significantly overpriced monetary policy tightening. Historical experience shows that after an oil supply shock, policy rates tend to rise slightly within one to three months but fall back within six to nine months as growth concerns intensify. He believes that the current inflation fears may prove excessive in the face of downside risks to growth and upward pressure on unemployment.

Bloomberg strategist Michael Ball summarized: “This is a transitional phase where markets are trying to shift from escalation concerns to patiently awaiting negotiations. Capital flows dominate everything, fundamentals take a backseat, and policy support has limited room. This combination points to a wider trading range at a lower level than before the Iran conflict.”

Editor/KOKO