{kind=link}

The Kotak report followed a promoter stake sale in June, after the end of the initial public offering (IPO) lock-in period, the chief executive’s resignation in October, and share offloading by Motilal Oswal Financial Services in November, further exacerbating negative sentiment. The stock has now fallen nearly 50% from its October peak.

Is this an opportunity to buy the leading electronics manufacturer, or a falling knife that investors should steer clear of?

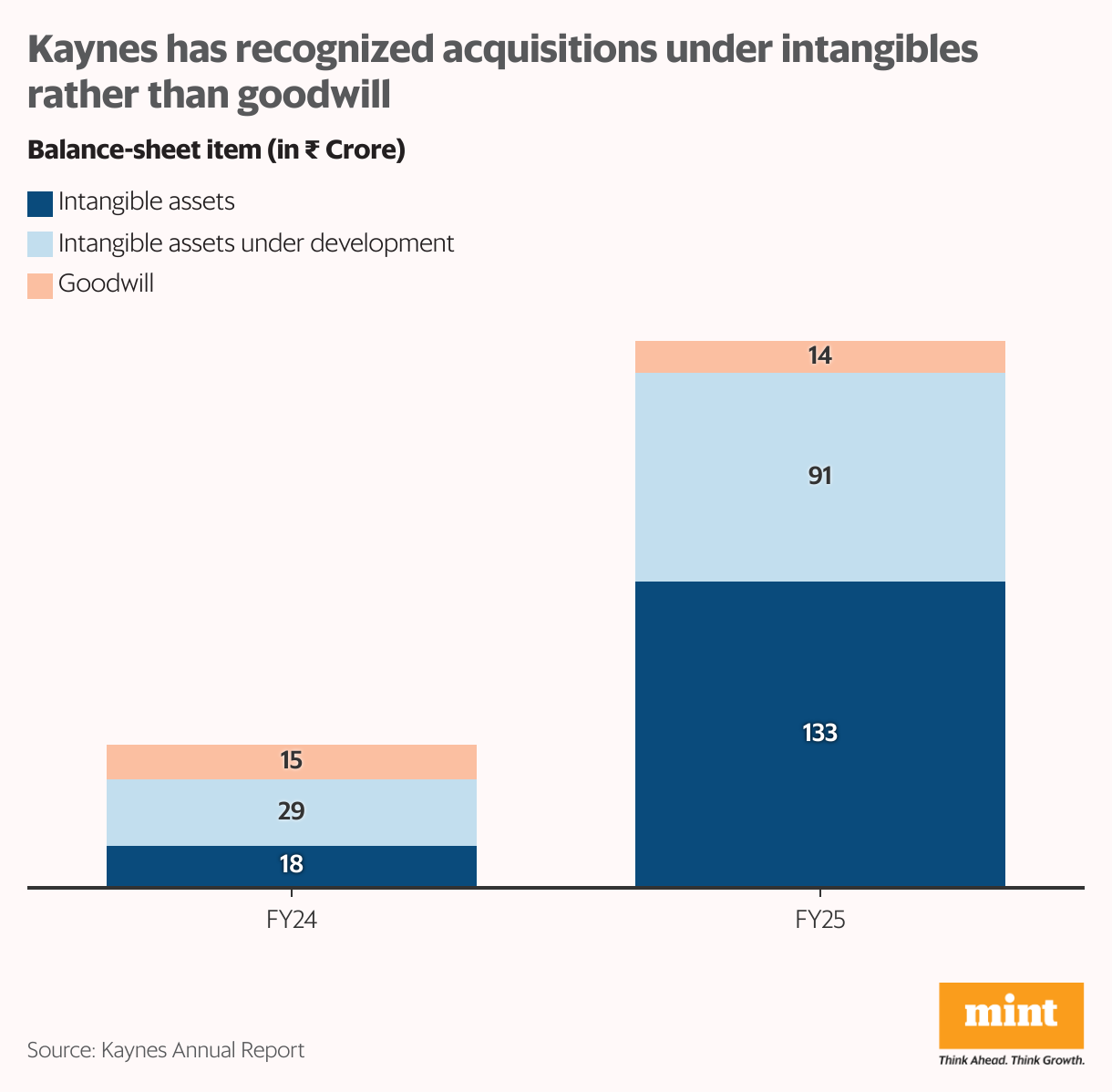

Is Kaynes’ accounting of acquisitions “ambiguous”?

Kaynes acquired Iskraemeco and a 54% stake in Sensonic for a consideration of ₹88 crore. However, the Kotak report has alleged that this acquisition doesn’t properly reflect in the company’s investing cash outflows or its goodwill on the balance sheet.

Also Read |

Four solid small-caps trading up to 60% below their 52-week highs

Kaynes’ management has clarified that the bulk of the consideration for the acquisitions was towards a large customer contract. So, it has been classified as an intangible asset to be amortized over the contract’s term, rather than as goodwill. Given the systematic amortization schedule followed for intangibles—as opposed to the discretionary, impairment-based treatment for goodwill—Kaynes’ approach appears more conservative.

The recognized intangible assets were netted off against goodwill, according to the management. As for cash flows, the company appears to have categorized them under capex-related cash flows, rather than acquisition-related outflows. At worst, this looks like a mis-categorization, rather than an attempt to mislead investors.

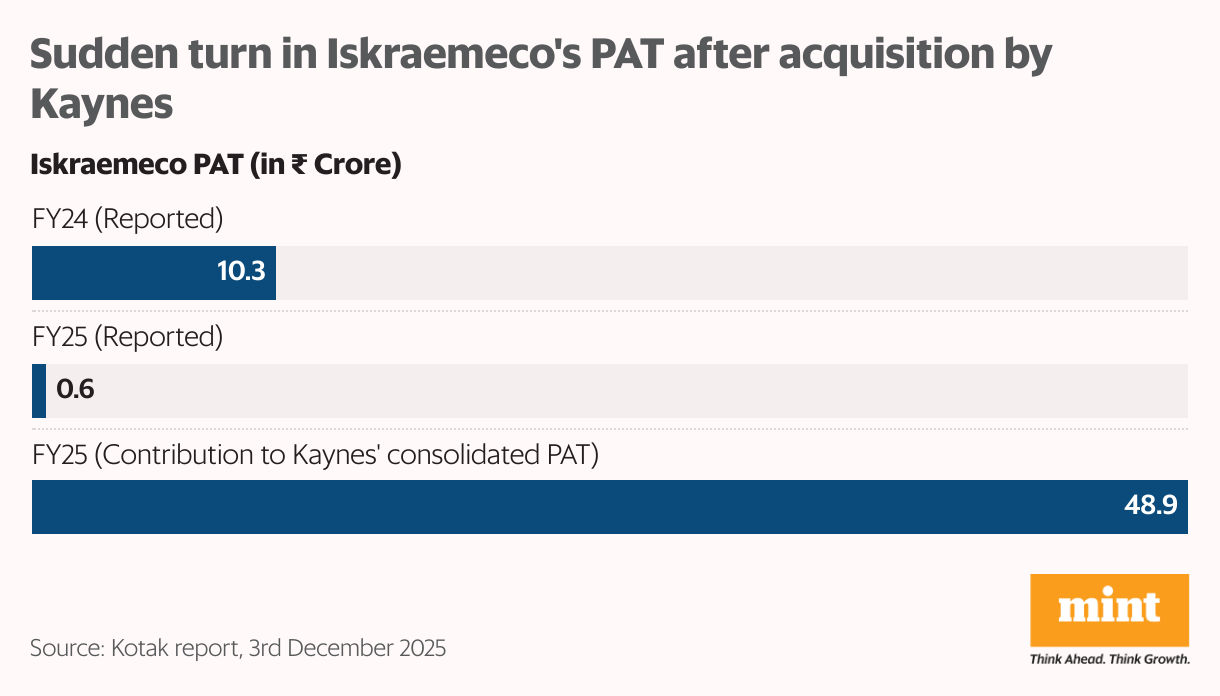

What about Iskraemeco’s sudden turn in fortunes?

Kotak’s report pointed out the ₹0.6 crore profit after tax (PAT) reported by Iskraemeco in 2024-25, which stands in stark contrast to its ₹48.9 crore contribution to Kaynes’ consolidated profit during the fiscal. Considering that Kaynes acquired Iskraemeco on 30 September 2024, it can be inferred that Iskraemeco went from reporting a ₹48.3 crore loss in the first half to a ₹48.9 crore profit in the second half. This conveniently timed turnaround in Iskraemeco has raised eyebrows.

Kaynes’ management has clarified that Iskraemeco’s loss in the first half was on account of the write-off of outdated inventory amounting to about ₹50 crore. This, along with low revenues amid continued fixed costs, had led to the losses during H1FY25. This also explains the net negative assets of Iskraemeco at the time of its acquisition. The management has also corrected Kotak’s estimate of Iskraemeco’s margin from 28% to a more palatable 9%.

Following the acquisition, Kaynes has provided corporate guarantees against funding requirements at Iskraemeco and other subsidiaries to support their business needs. This has helped Iskraemeco clock higher revenues and profits in H2FY25, but has also led to higher contingent liabilities reported by Kaynes. Kotak’s analysis pointed out the spike in contingent liabilities from ₹270 crore in 2023-24 to ₹520 crore in 2024-25.

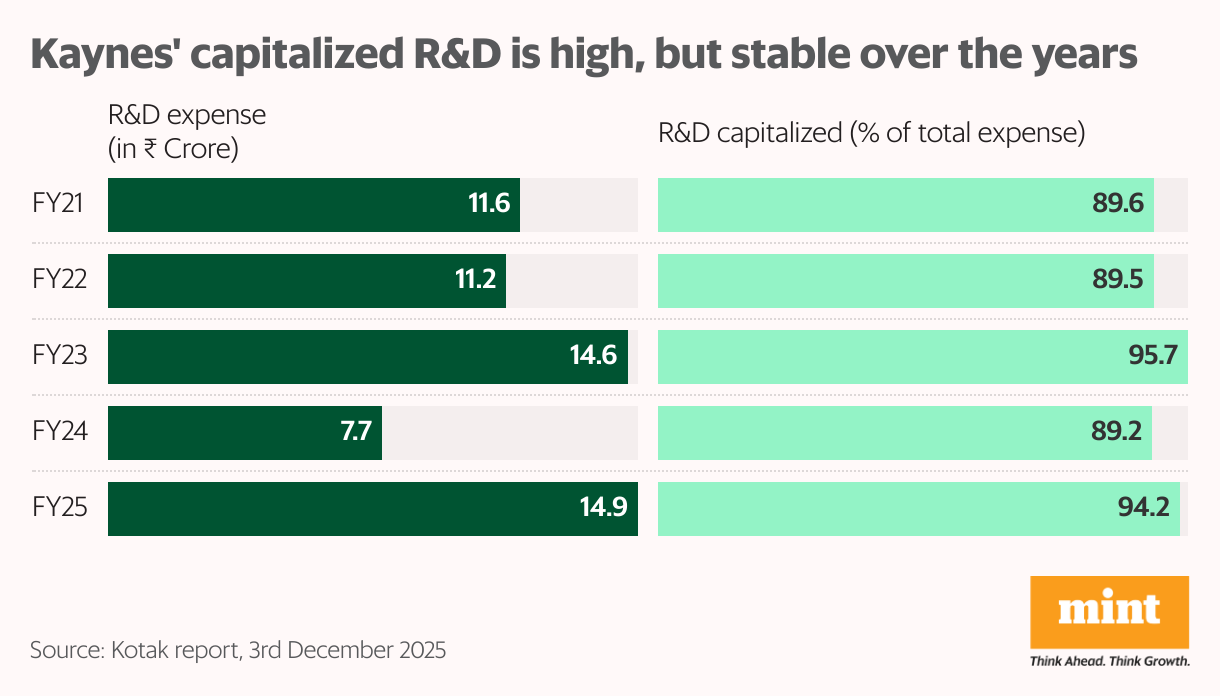

What about R&D capitalization and high borrowing costs?

The Kotak analysis showed that 94% of research and development (R&D) expenses incurred by Kaynes were capitalized in 2024-25. The management has elaborated on its R&D accounting policy—experimental R&D expenses are recognized on the P&L, while those expected to result in a revenue stream are capitalized. They have pointed to how heavy R&D is critical to the nature of the business, and that the mix of expenses versus capitalization has remained largely consistent over the years.

Also Read |

As NephroPlus expands abroad, scale turns into its toughest test yet

As for the concerns raised about the high cost of borrowing, calculated at 17% in Kotak’s report, the company has attributed it to the simplistic method of calculation. Including bill discounting, the cost of borrowing would come to about 10%, according to the management.

Have there been any lapses in disclosures?

The company has admitted to inadvertently missing out on reporting related-party disclosures in its subsidiaries’ standalone statements. The missed disclosures pertain to Kaynes Technology and Kaynes Electronics Manufacturing’s transactions with Iskraemeco. The management insists that the underlying financials and schedules include all the necessary details.

It has taken steps to avoid such lapses in the future, including connecting its ERP systems to its financial statements with limited manual intervention. It has also vouched to improve shareholder communication, even as reports suggest a possible change in its auditor.

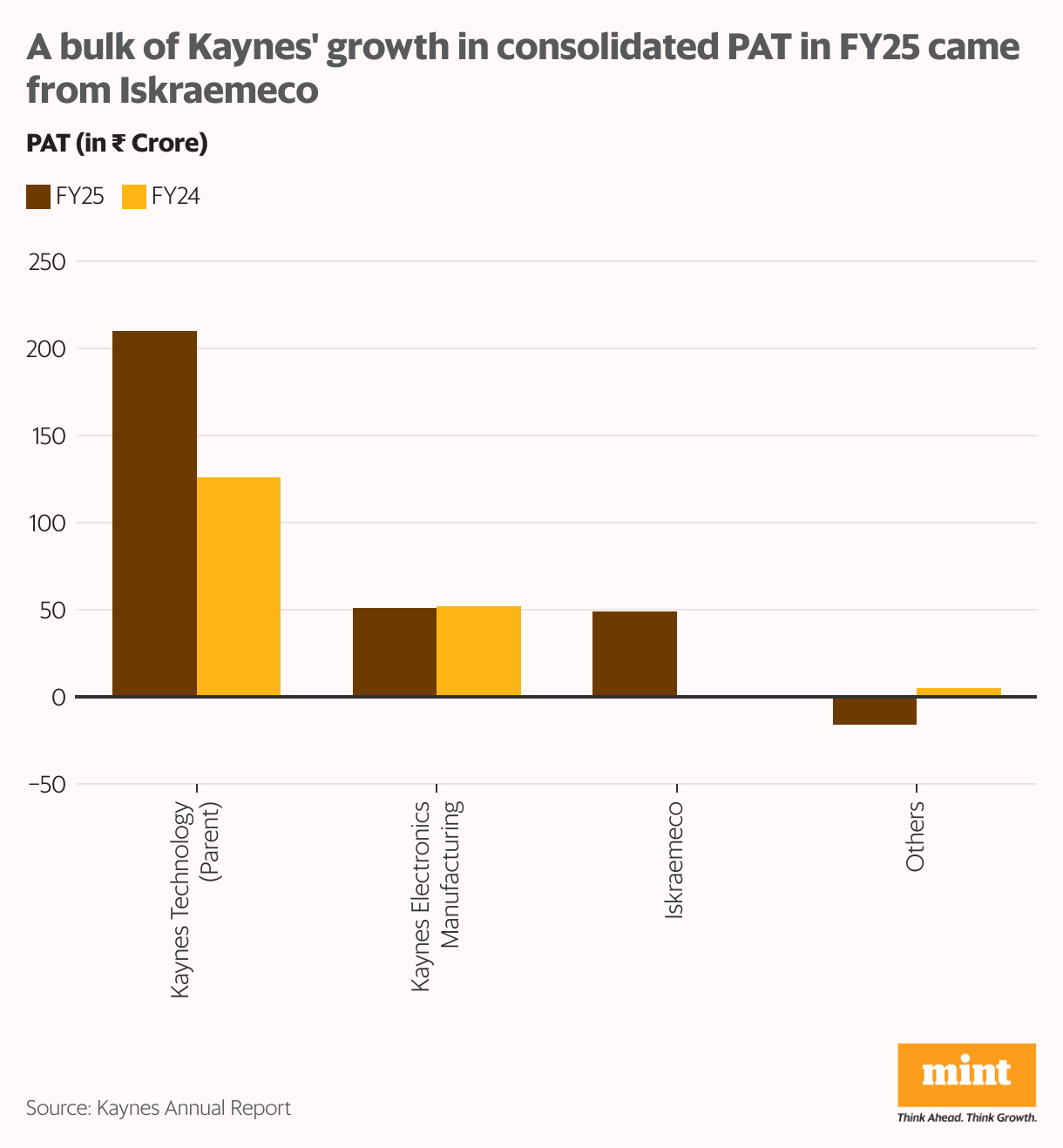

What about Kaynes’ growth prospects?

While the management has clarified most of the questions raised by Kotak’s analysis, concerns about business fundamentals persist. Despite robust growth reported in recent quarters, a look under the hood reveals that profits from the Iskraemeco acquisition contributed around 44% of the profits added by Kaynes in 2024-25. This indicates slow organic growth in its core electronics manufacturing (EMS) business.

The management has assured investors that it will remain focused on core EMS, and core growth is expected to surpass that of tangentially related subsidiaries. They have acquired marquee customers in electric vehicles, and have also bagged orders for Indian Railways’ Kavach programme, and aerospace and defence orders from original equipment manufacturers.

But its Outsourced Semiconductor Assembly and Test (OSAT) and printed circuit board (PCB) forays are yet to yield tangible results. The management pointed to three clients acquired in the space, but admitted that waiting for client approvals could lead to revenue recognition being delayed beyond the initially provided guidance. The proof will be in the pudding, and the company’s core organic growth in subsequent quarters will be closely watched.

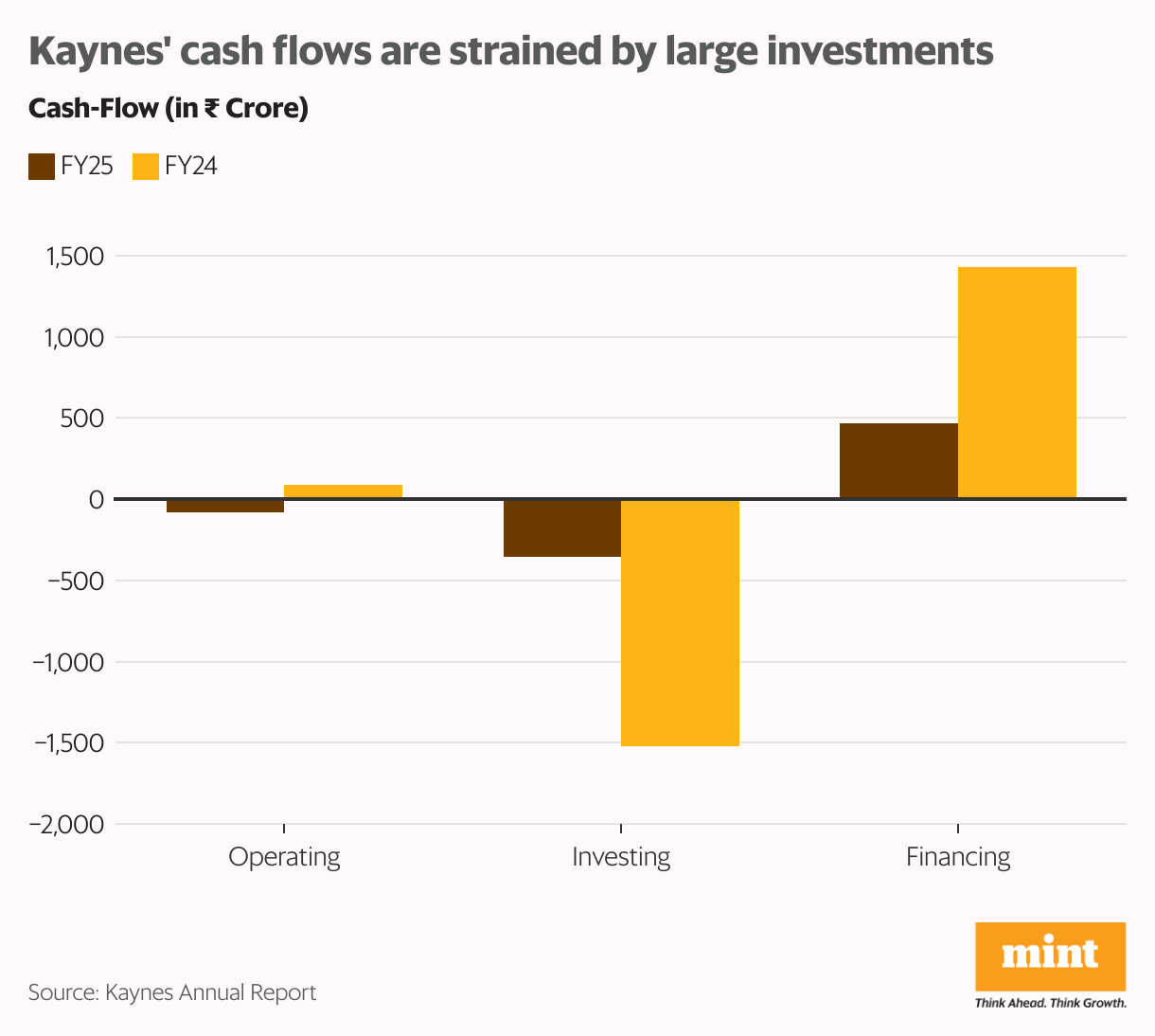

Are there concerns about Kaynes’ cash flows?

Kaynes’ strained cash flows raise a large question mark on its fundamentals. Its cash-flow conversion expanded from 135 to 157 days in 2024-25, and is expected to remain strained due to heavy capex requirements. The management has acknowledged that free cash flows may not turn positive any time soon, despite positive operational cash flows.

Making matters worse, debtors and doubtful debt have grown. As of 2025-26, quarterly revenues have remained stagnant, while debtors have almost doubled to ₹1,120 crore, and the company has provisioned ₹55 crore towards doubtful debt. Kaynes’ payables due to Iskraemeco worth ₹46 crore have also been due for over a year, which it hopes to clear by the end of this fiscal.

The management has called this out as an industry-wide phenomenon, while remaining hopeful of recovering the doubtful debt and reversing the provisions in subsequent quarters. But investors should go by tangible improvement on the ground, rather than promises of recovery.

Out of about ₹700 crore in receivables at Iskraemeco, the management aims to discount about ₹250 crore over the near term. It also plans to gradually transition its subsidiaries from device manufacturing to product solutioning, which should relieve some of the strain on working capital. As for delays in government grants and subsidies, the company has tasked a team to smoothen its transactions with the government. It does not expect any strain on project execution or on its books due to delays in government receivables.

Detailed queries sent to Kaynes remained unanswered until press time.

Are there any silver linings?

Amid talks of required capital infusion, the management has assured that the company neither needs nor plans any promoter dilution in the near term. The stock can also draw technical support from its critical support level around ₹4,000 apiece.

Also Read |

Indus Towers stock: Recovery story or value trap?

After the recent sharp correction, it is trading at a palatable price/earnings-to-growth (PEG) ratio of 0.8x that leaves room for upside once the Street is satisfied with the management’s responses to Kotak’s implications.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment adviser. X: @ananyaroycfa

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.